A "Miner" Adjustment

Bitcoin's fast approaching halving is going to have an impact in the mining space. I like three different names; a monster, a takeover target, and a small cap spec.

We’re roughly 4 or 5 days away from Bitcoin’s block reward halving. Have you guys heard of this? I kiid. Anyway, in classic crypto fashion it looks like there’s a chance the halving will be on 4-20… if the price of BTC is “69” thousand dollars at the same time then we’ll officially know this whole universe is a giant meme. There are actually a lot of you who have subscribed in the last few weeks so it’s possible the concept of the Bitcoin halving cycle is foreign to you.

I’ll now attempt to briefly summarize what this means before jumping into the real meat of the post. If you already get it, feel free to jump to the next section.

Bitcoin Halving Explained

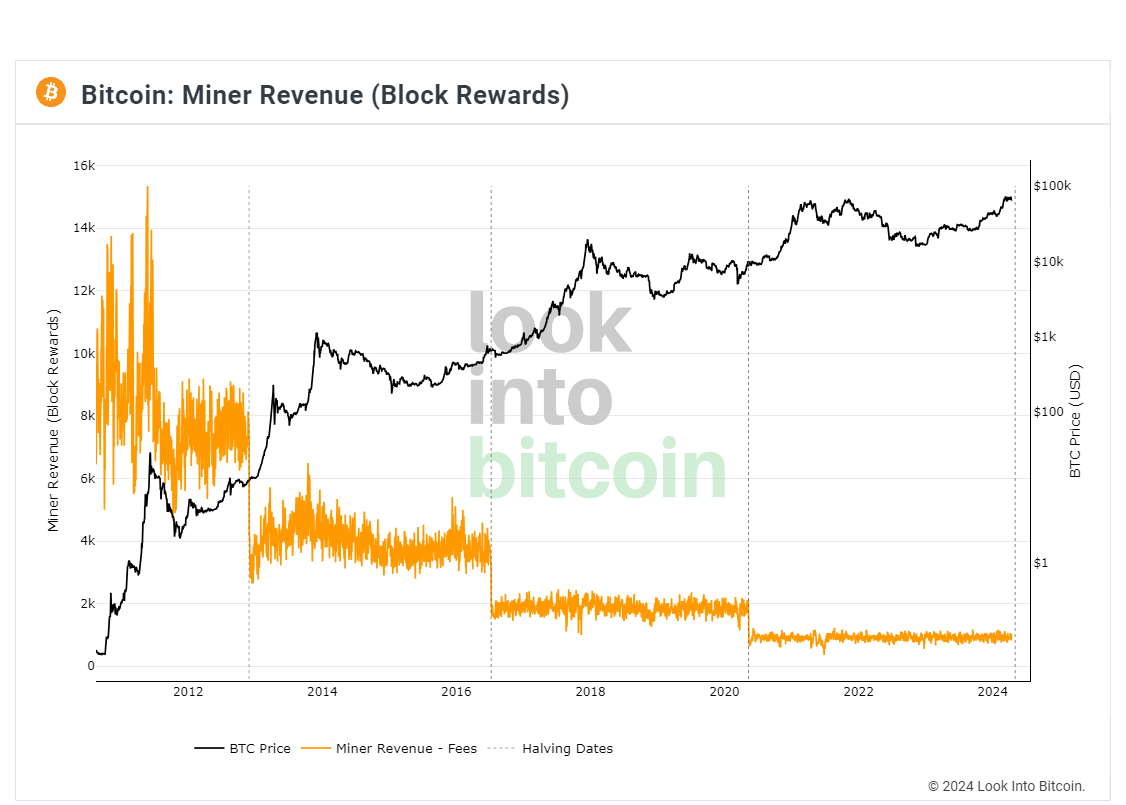

Bitcoin was designed with a fixed supply of 21 million coins. This is a coded hard limit to the amount of BTC that will exist on chain - thus, the perception that BTC is a “store of value” due to it being the first truly scarce digital asset. There are about 19.7 million coins already in circulation and the remaining 1.3 million will be issued over time as new blocks are created on the blockchain. Computers, or “miners,” are rewarded with the new coins when they validate transactions on the ledger. Today, there are 6.25 new BTC issued through each new block. Next week, that figure will be down to just 3.125.

The newly issued coins, sometimes referred to as the block reward subsidy, are trimmed by 50% about every 4 years. Each time this has happened in the past, the price of BTC has gone into a mania that takes nominal BTC price to a new high. Why does this happen? To me, it’s equal parts supply crunch meets FOMO. The less BTC generated by the block reward subsidy, the less sell pressure from miners selling BTC to cover operational costs. So if demand from the public stays the same but supply diminishes, BTC rerates higher.

Validation Incentives

The halving has historically been a major bullish catalyst for the price of Bitcoin. How one views this block reward/halving dynamic is certainly up to interpretation. To make up for an ever diminishing block reward subsidy, it has become borderline essential for much higher coin prices so the miners continue to have an incentive for validating on-chain transactions. This is not a sustainable trend in my view. Mining BTC requires equipment and energy - neither of which are free.

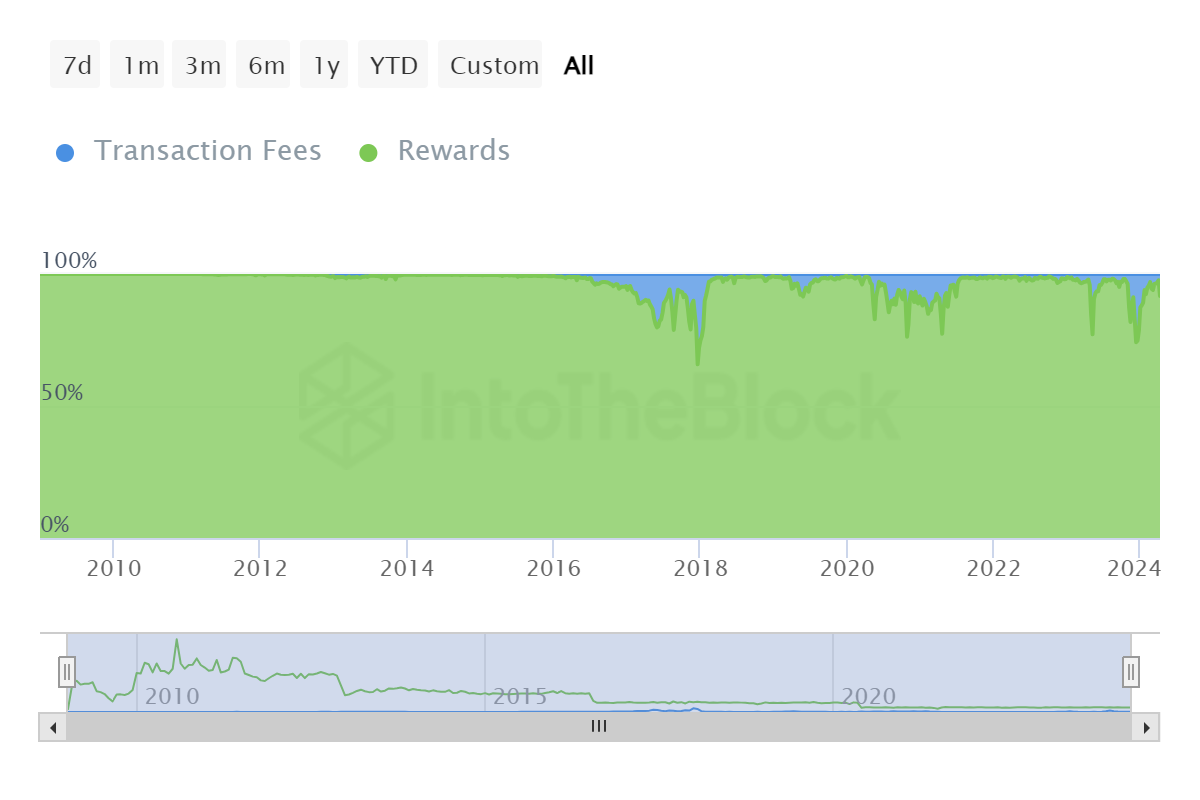

Thus, an alternative incentive for transaction validation is required. This is why many other blockchains don’t require miners at all and are instead validated by a proof-of-stake model rather than the miner-driven proof-of-work model. No matter which model a chain creator chooses, if coin supply has a hard cap, transactions will ultimately have to be funded by usage fees.

Given the fact that the block subsidy will inevitably stop printing new BTC, I think it’s pretty clear that transaction fees will have to become a viable incentive mechanism for validation in the future. Otherwise, the security of the network is at a significant risk. Bitcoin has an absolutely enormous advantage in the zeitgeist. Even though there are other coins that are currently more profitable to mine, the computing power is almost all still backing BTC.

To be clear, I’m not going to sit here and make the claim that Bitcoin miners are going to all flip to Bitcoin Cash post-halving because they’ll make more money. But I will sit and here and make the claim that some of them probably will. Because the alternative is mining at a loss or simply not mining at all. Especially if the price of BTC comes down - which has been happening in recent days.

BTC at $52k out of the question? I think not.

Industry Consolidation?

One of the great things about the halving for miners is it’s a well-telegraphed event. If you think the market hasn’t already been pricing this into the two dozen or so public BTC mining companies yet with less than a week remaining, I’d be willing to take the other side of that argument.

Consider the price performances of Bitcoin compared with the public mining equities as expressed by the Valkryie Bitcoin Miners ETF WGMI 0.00%↑ - with a couple of notable exceptions, the miner group peaked in December when Bitcoin was $42k. Traders would have done a hell of a lot better flipping from miners to BTC near the end of 2023 rather than riding the mining shares down, or worse, chasing miners at the highs…

What I think we’re about to watch now is consolidation within the field where well capitalized miners that have hoards of cash, BTC, and minimal debt will be able to wait out any post-halving coin price bleed and possibly even buyout peers that can’t efficiently compete any longer. So who is left standing when the dust settles?

Names Still Worth Holding?

For the last 12 to 18 months, I’ve been pretty clear in my writings both here and on Seeking Alpha that I don’t think most of these businesses are viable long term. Great trading vehicles for sure. Great investments? I’m not convinced. Given that, I think a lot of these equities may get knocked down even further if/when BTC moves lower post-halving.

In my SA work, I’ve been sharing my back of the envelope estimate for breakeven price. My breakeven price adds cost of revenue to total operational expenses and divides that figure by the BTC mined in the quarter. This is what these figures are in the names I currently track:

There are just two companies from the ten selected that are profitable post-halving at today’s BTC prices. Those are TeraWulf WULF 0.00%↑ and Bit Digital BTBT 0.00%↑. Marathon Digital MARA 0.00%↑ is close at $70k. Riot Platforms RIOT 0.00%↑, CleanSpark CLSK 0.00%↑, Bitdeer BTDR 0.00%↑, and Hut 8 HUT 0.00%↑ need six-figure prices to be viable. I suspect these high cost miners will either have to merge with other companies the way HUT did last year, or buyout smaller firms with better fleets. RIOT should be active in my view.

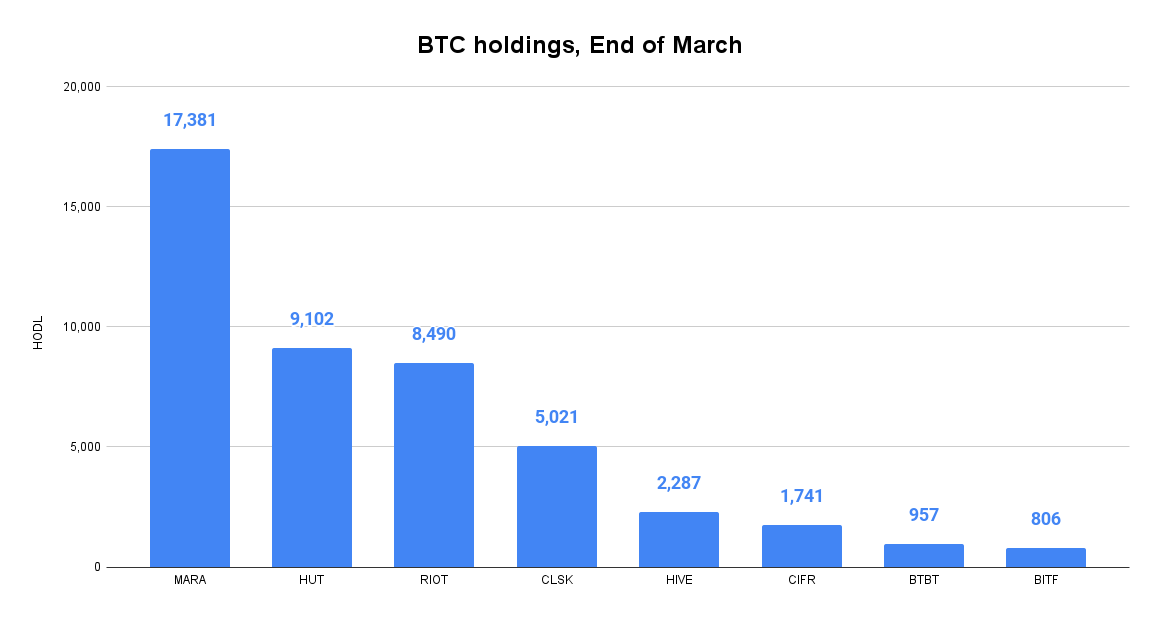

This is how the BTC treasuries shake out as of end of March:

MARA is without question the best-equipped to weather any short term storm given the company’s BTC liquidity. Despite the large stack, HUT is borderline untouchable due to its debt load alone. The company is bordering on distressed and is already making changes as evidenced by a new CEO and a site closure that resulted in a 25% reduction in March exahash capacity:

On March 6, we announced the closure of Drumheller. Our team relocated efficient miners to Medicine Hat and retired inefficient miners. We expect to see the impact of these changes on our operating efficiency moving forward.

Even though Bit Digital has a far smaller stack compared to the rest of these miners, the company also has an Ethereum strategy and appears to be the only company in this table above that is making meaningful strides in HPC as an alternative revenue stream:

Like CleanSpark, BTBT has virtually no debt. The company that is really interesting as a potential takeover target is TeraWulf. They’ve been selling all production each month, aggressively paid down debt, and have built what is likely the most efficient fleet in the industry. They have no HODL, but could certainly pivot to stacking if they want to given my breakeven estimates.

Personally, I’m much less excited about CleanSpark going forward. That breakeven price is a bit of a concern and I suspect there will be a bit of dilution coming. Retail now loves this name and that makes me nervous. All of these companies dilute, but compared to MARA and RIOT, CLSK has less BTC to deploy in a pinch. CLSK is also one of the only equities that hasn’t given up its 200 day MA yet and I suspect there could be more downside there than elsewhere if we see a deeper BTC correction as it will “catch up” (or catch down).

Something else that is interesting about Marathon Digital is it has its own pool that allows users to go direct with fees. For example, if I have a high value transaction and I want assurance that it will clear, I could pay a larger transaction fee than average and go direct to MARA to validate. This appears to be happening more. Over the last 3 months, MARA’s pool is generating more than the expected block return from fees while the other pools underperform. It’s early and this is a small sample size, but I think this is a really interesting development.

So today, I’m long three of these names:

MARA, BTBT, WULF.

MARA is the monster. WULF is the takeover target. BTBT is the small cap spec. If my perspective changes, I’ll certainly share. But for now, I’m comfortable going into the halving with these three stocks.

Disclaimer: None of this is investment advise. I share what I do and why I do it for informational purposes.