Financial Nihilism, Hijacking Bitcoin, & Crypto Portfolio Strategy in 2024

In a market driven by narratives over substance, is there any room for a fundamental approach to investing in innovative technology? Some say no. I say yes.

There’s not enough meat left on the bone in BTC and ETH. Moreso in BTC because once you get to prior all time highs, lets just call it $70k for round numbers, how much more are you going to get from that? You going to get a double? $140k? You going to get a triple? That just feels like a little bit of a stretch. And that’s just not enough. People aren’t in this thing for a double. - Travis Kling via The Grant Williams Podcast

That’s an incredible quote to me. I’ll unpack it more in a bit but first I would encourage all of you to listen to the entire episode from which it came. Grant’s podcast is typically paywalled but he occasionally lets a full episode hit the feed on the house every now and again:

The reason this episode happened is because Travis Kling went viral on Twitter in February for essentially making the argument that crypto isn’t saving the world and has no real fundamentals. In his view, despite those issues, it’s okay to keep taking shots in this space anyway because the number keeps going up and will likely continue to do so. I don’t think he intends for his message to come across this way, but it’s a fairly depressing read.

To be clear: I don’t actually disagree with most of it and you’ve likely seen my lamenting many similar points on this blog for some time. For example, I drew a connection between crypto and Christopher Lunsford (aka Oliver Anthony) in Selling Your Soul In The Era of Social Degradation last August:

I can’t help but notice the absurdity of the juxtaposition in this moment. The distributed ledger technology that came with the emergence of Bitcoin is supposed to address the inequalities that people like Lunsford sing about. Yet in common practice, too many in the industry seem more enthusiastic about using the technology for riding the next speculative frenzy rather than for empowering publishers and creators. - August 2023

Kling also connects crypto to Lunsford in one of his threads though he comes at it through a different angle; Lunsford’s popular song “Rich Men North of Richmond” is a byproduct of the same issues that have led to wild speculation in crypto. His thinking goes something like this; the young people who are into crypto are in it because they view coins and tokens as lotto tickets in a broken system. For them, the possibility of 2x or even 3x returns from the more mature assets like BTC and ETH simply isn’t good enough because a 2x on a $1k investment isn’t life changing but a 1,000x on the same money would be.

Thus, tokens like “Bonk” and “dogwifhat” have gone ballistic while other assets with “fundamentals” don’t generate even close to the same kind of returns. If I can critique Kling’s nihilism thesis slightly it would be to say this; not everyone in this market is chasing 1,000x returns so they can buy a “Lambo” and pretend they’re happy. Even though my tone on this blog is often nihilistic highly sarcastic, I am actually very optimistic that this technology can legitimately solve problems even though it hasn’t really happened at scale yet. However, I can also admit that as a Millennial homeowner with a wife, kid, and plenty of weekend free time, I’m probably not in this for the same reasons as those who aren’t as fortunate as I am.

The real meat and potatoes driving Kling’s thesis though came in his follow up thread last month which aims to explain the “why” that is driving all of the nihilism. As I’m sure many of you can probably guess, a big catalyst behind the financial degeneracy has been monetary policy and the lack of total wealth share held by the Millennial generation.

Those individuals choosing to act out Financial Nihilism are doing so in direct response to, and in imitation of, the monetary and fiscal policies of the Fed and the US government. Those monetary and fiscal policies have been a major driver of wealth inequality both through generations and wealth percentiles. The US government has been egregiously irresponsible. Makes a poker player look like Dave Ramsey. - Travis Kling

Well put, in my view, and I think Kling’s rundown of what drives all the wild casino behavior in crypto is excellent.

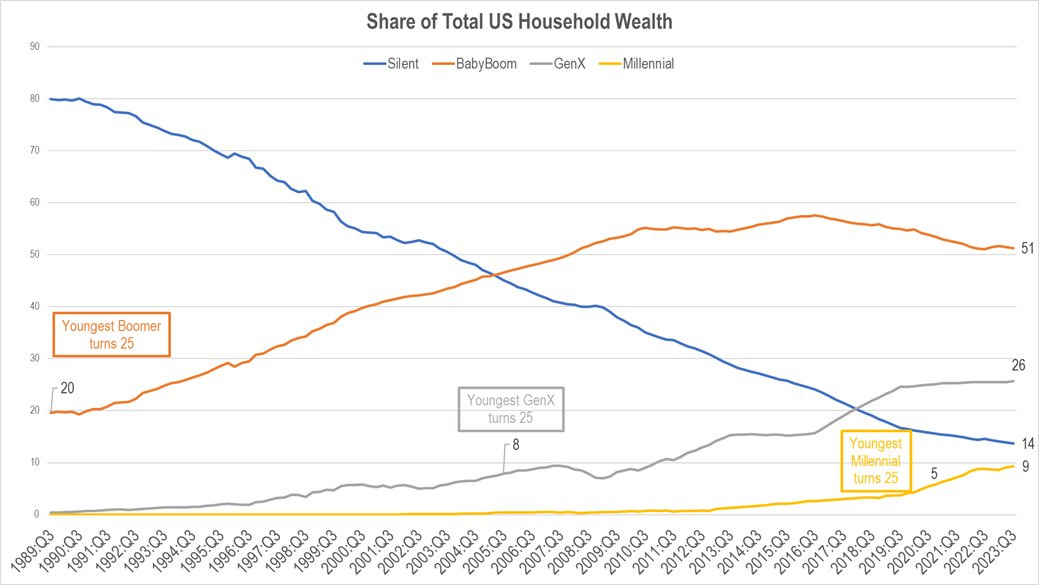

We can look at charts like this one that specifically target share of real estate or share of stock market equity, but the simplest way to drive home the point is total household wealth in America. When the youngest Boomers turned 25 years old, the Boomer generation held 20% of US HH wealth share. Millennials are still at just 9% even though the youngest of that generation turned 25 several years ago. This is not meant to be a Boomers vs Millennials point. It’s just the macro setup that we’re in and it helps to explain the nihilism - of which, chasing risk in crypto is a symptom not a cause.

This is not the fault of Boomers, for what it’s worth. Everyone in this world is just playing the hand they’ve been dealt. And whether they realize it or not, the reason one generation has such a large share of wealth is because they’ve all been unknowingly pushed out on the risk curve as well. The only difference is 401k contributions don’t feed passive fund flow into “Bonk” or “dogwifhat.” But make no mistake about it, very few in this game we call investing are actually liquid and for every ridiculous memecoin with a top 50 crypto market capitalization there’s a Mag7 stonk trading at a 35+ trailing price to earnings multiple waiting to get punished. We’re all just traders playing the ponies, some of us may just be more aware of it than others.

But bringing it back to the opening, there’s a very important point from Kling’s Grant Williams podcast quote that I opened this post with that I think requires reinforcement; the price of BTC may not actually go as high as many in the market expect it to precisely for the reason he laid out. Is 2x not good enough anymore? I suppose we’ll find out. There could actually be some merit to the idea that BTC gains from here will be well below expectations. Most of the Boomers that I know have essentially zero interest in “Bitcoin” whatsoever or “crypto” if you subscribe to the notion that they’re somehow different things. All of this brings us to a possibly inconvenient truth about BTC that is as important to explore as it is timely.

Hijacking Bitcoin: The Pivot From “Peer To Peer” to “HODL”

Over the weekend I read Hijacking Bitcoin by Roger Ver and it’s a fantastic read that I highly recommend. Look, if you’re a BTC Maxi, you’re not going to like it as it’s going to challenge many of the narratives that have driven BTC to a price of $70k. But I suspect if you’re a Maxi you’re probably not even reading this blog, so I digress. Before reacting to the book specifically, recall my thinking shortly after FTX collapsed:

We trust ourselves to operate motor vehicles at high speeds at night but we can’t trust ourselves to store 12 words on a piece of paper? I refuse to believe the majority of the populace lacks the competence to custody crypto without an intermediary. We should expect more of ourselves. FTX customers didn’t lose their savings because Bitcoin or because some other crypto network failed; they lost their savings because they trusted a third party when they didn’t need to. - November 2022

I complained about lamented people keeping their crypto assets with exchanges when the entire point of all this is for these assets to be directly held on-chain. And in the 18 months since, we’ve completely jumped the shark in the pivot from BTC being a self-custody asset to being hoarded for capital gains. It’s gone a step further. Now retail buyers aren’t even buying BTC through an exchange and simply leaving the coins there; they’re buying through a traditional financial product offered by BlackRock BLK 0.00%↑ that settles redemption requests in USD rather than in-kind. To call this a divergence from Satoshi Nakamoto’s original white paper would be an understatement.

BTC still works wonderfully as a self-custodial asset. The problem is that actually using Bitcoin for it’s intended purpose is becoming as out of reach for most people as real estate for a Millennial. Want to take delivery of $25 worth of BTC to a self-custodial wallet? Forget about it. The fee to transact takes 20% right off the top:

If you intend to transact twice, your “store of value” is down 40% and this assumes fees don’t increase from $5 per transaction. Given the block reward is halved every 4 years, miners will inevitably need real usage and real fees to incentivize network security. This is a very legitimate long term concern that BTC bulls have been handwaving away due to potential scaling through centralized vaporware secondary networks and side chains. Of course, if the base layer of the Bitcoin blockchain wasn’t still arbitrarily constrained by a small block size relative to peers, transactions could scale directly and miners could be paid by a larger volume of small fees rather than small volume of high fees.

As it stands currently, most users have been priced out of the network entirely. Again, Bitcoin was designed to be a network for peer to peer value transfer and the current BTC iteration of that idea simply hasn’t achieved that - masking this failure has been the narrative shift from “digital currency” to “digital gold.” For years, I have been frustrated at this narrative pivot from utility to hoarding. You can check the receipts:

Sure, I’m still plenty exposed to BTC for the “number go up” gains. But I suppose that’s just the financial nihilist in me. All that said, what I was much less aware of before reading this book is just how brutal the Block Size War actually was and Roger Ver’s perspective on that time is quite eye-opening to say the least.

The war was far more than just a simple difference in ideological belief about nodes and block sizes. As he puts it, the big blocker camp that inevitably forked and became Bitcoin Cash ($BCH-USD) battled censorship on platforms like Reddit RDDT 0.00%↑, DDoS attacks, and a loss of confidence from several early Bitcoin developers including Mike Hearn and Gavin Andresen, who Satoshi Nakamoto picked as successor to lead development.

In the book, Ver insinuates that Bitcoin’s pivot from peer to peer payments to “digital gold” was largely aided by intentional sabotage from developers like Peter Todd - who as fate would have it, also took part in the original Zcash ($ZEC-USD) launch ceremony before almost immediately FUDing the project — Ver on Todd’s role undermining Bitcoin:

“John Dillon” is the pseudonym of an unknown person who paid Peter Todd, a Core developer, to produce a video promoting the restriction of Bitcoin’s throughput to seven transactions per second. He offered a bounty to develop replace-by-fee, which was intended to “break zero-conf security now”—that is, to break the functionality of instant transactions. Gavin Andresen publicly speculated that Dillon had an ulterior motive to destroy Bitcoin, and later it turns out, in leaked emails, that Dillon claimed to be in a high position within an intelligence agency. - Hijacking Bitcoin, Page 125

This is the video referenced in that excerpt from the book:

I encourage you to read the comments as they’re all generally from that time period and reflect a very different kind of sentiment from the consensus that small blockers claimed the broader community had. Ver closed that chapter of the book by saying:

All of this happened around the most revolutionary financial invention in history, which directly challenges established governmental, financial, and banking powers around the world. Readers can come to their own conclusions, but in my mind, by late 2013, Bitcoin had already been targeted for capture. - Hijacking Bitcoin, Page 125

All of the intrigue of intelligence agency sabotage aside, I think my biggest takeaway from Roger’s book is the bigger Bitcoin became, the more it likely suffered from a governance structure that appears to have lacked resiliency. Satoshi Nakamoto left the keys to the kingdom in the hands of Gavin Andresen, who doesn’t seem to have actually wanted them. Ver put almost all of blame for the block space war on Bitcoin Core and BlockStream, the primary developers maintaining the network. But Mike Hearn’s 2016 essay seems to throw a considerable amount of shame on China-based miners:

Chinese internet is so broken by their government’s firewall that moving data across the border barely works at all, with speeds routinely worse than what mobile phones provide. Imagine an entire country connected to the rest of the world by cheap hotel wifi, and you’ve got the picture. Right now, the Chinese miners are able to — just about — maintain their connection to the global internet and claim the 25 BTC reward ($11,000) that each block they create gives them. But if the Bitcoin network got more popular, they fear taking part would get too difficult and they’d lose their income stream. This gives them a perverse financial incentive to actually try and stop Bitcoin becoming popular.

At that time, Bitcoin’s hash power was dominated by Chinese mining pools. Miners had the ability to take power away from Bitcoin Core developers had they chosen to do so but Hearn contends they decided not to because it wasn’t in their financial interest.

All of this may paint a fairly damning picture for BTC. And I’ll be very clear that I do have serious doubts about the sustainability of the longer term trajectory the network is on if dramatic changes aren’t made to either the block size limit or miner incentives. It’s also very important to reiterate that Roger Ver supported Bitcoin Cash during and following the BCH fork. Some may point to this book as sour grapes that BTC is the network that has enjoyed mainstream success as both a “store of value” idea and as a driver of capital gains. But I personally disagree with that argument and Roger still owns BTC and was already wealthy before he became a Bitcoiner.

Still, what should be our main takeaway from all of this? Naturally, my view is that you should form your own view. Does this all mean one should sell all their BTC because the network hasn’t functioned the way Satoshi envisioned? Not at all. But I do think it helps justify a multi-coin approach to cryptocurrency holdings. In a market that is open 24 hours a day, 7 days a week, discovery is never over.

Crypto Portfolio Strategy

I’m still very optimistic about the future of peer to peer payments without intermediaries. I’m also still very optimistic that blockchains can do more than just payments. I humbly reject the notion that 2024 crypto investment should be about buying the silliest tokens possible and simply riding memes and jokes. One can certainly trade that stuff if that’s how they want to spend their time, but in a serious world I still believe utility ultimately wins over speculation when it’s all said an done. And perhaps it’s blind faith at this point, but I still believe the end result of all of this technological experimentation is the inevitability of anti-state money:

These things take time. I’ve certainly had to manage my own frustrations with utility and scaling. But these networks are inevitable and there is no putting web-based money back in the bottle. It’s here. We should use it. - May 2023

I’ve personally tried what I would call an “over-diversified,” fundamental approach to altcoins and digital assets. This has admittedly not worked in my favor. When I was operating the BlockChain Reaction crypto research service through Seeking Alpha between May 2022 and May 2023, I labeled 25 altcoins to be my “top token ideas,” or TTIs. Here’s a fun stat, an equal weighted portfolio of those coins would currently have a total return of about 175%. Sound good? What’s our benchmark?

Had the capital that went into those altcoins gone into Bitcoin instead as part of a single-asset dollar cost averaging strategy, that total return would have been 215%. All that work. All that research. And just buying BTC instead would have produced better returns. Obviously, I find this to be frustrating for a variety of reasons. Perhaps because even before Hijacking Bitcoin, I found the pivot from P2P value transfer to be a blatant contradiction of the cypherpunk ideals that spawned the network in the first place. Or perhaps there is an ego component to this as well; I’m admittedly peeved that the digital version of the pet rock is beating all my “bright ideas.”

Of course, the verdict is certainly not out yet on many of those altcoins that I highlighted but I can’t help but view my portfolio strategy during the BCR days as more of a failure than a success. And I hold this view for three critical reasons:

Proof is in the pudding; my old approach underperformed.

Token-economic models aren’t always necessary.

It may be better to know 5 to 10 networks/coins really well than to force an understanding of 25-50.

The good news is, failures are only failures if a lesson isn’t learned. I enjoyed doing all of that research. That was without a doubt beneficial to helping me develop my personal process. And after having tried it, I now believe exposure to dozens of different altcoins in an attempt to find “the gems” is probably the wrong way to go about crypto portfolio building. To be clear, I don’t think there’s anything wrong with alts, I just wouldn’t over-diversify.

That said, no single portfolio strategy works for everyone. For those who want exposure to crypto simply for potential lotto-like gains and nothing more, have at it and keep doing you. But if one wants to get beyond memes and explore ideas that could have a more lasting impact, I think each investor has to ask themself a critical question:

What do I want this technology to do for me?

Any real investor in this space should figure out what the answer to that question is and then go look for opportunities in that realm. Personally, I want decentralized systems to disrupt legacy media platforms and ad-based businesses. For that reason, I like the idea of token-gating, wallet-based sign-in, distributed data archives, decentralized social platforms, and of course… peer to peer payment infrastructure. At a time when Stripe can cause problems for Robert Malone’s Substack, the need for payment alternatives (and possibly “Web3” content distribution alternatives) is obvious.

One of the big reasons so many of my TTI picks are underperforming Bitcoin may be because the networks or applications underpinning the tokens either aren’t being used or flat out don’t require a token-economic model to exist at all. There’s probably no better example of the latter right now than the Basic Attention Token ($BAT-USD):

BAT is the token of the Brave ecosystem - the flagship product of which is the Brave Browser. I use Brave every single day. I actually really like it. Other people do too. The Brave browser had 26.3 million DAUs in March. As far as I can tell, this is one of the only “Web3” products that unequivocally grew usage throughout Crypto Winter and it flat out hasn’t mattered for the token’s valuation. Why?

Probably because the ecosystem doesn’t seem to actually need the BAT token to thrive - and this is the major flaw in any token-economic model that is shared by most of the tokens that I have analyzed on fundamental merits. This makes true “investing” in digital assets extremely difficult. As far as I can tell, the major function of the BAT token to this point has been as a vehicle for Brave’s ICO buyers to sell out to retail. This certainly doesn’t mean BAT can’t get a second life as an in-browser utility coin of some sort, and that’s clearly in the plan. Per Brave:

60 million monthly active users, 23 million daily active users, 1.8 million verified creators accepting BAT, millions of wallets created, thousands of ad campaigns with leading brands, and growing utility in the most innovative names in blockchain gaming. The results make BAT one of the most, if not the most, successful alt–coin projects to date.

Bold above my emphasis. One of the most successful alt-coin projects? I’d actually agree with that statement. Yet, the alt-coin itself has been a major disappointment. The question is what is the catalyst that reverses this? I suspect regulator clarity is currently the primary hurdle. And it’s going to likely take a dramatic shift in how congress and the White House view token-economic systems for token issuers and users to get that clarity. For now, BAT may not have the most compelling bull case - and I say this with BAT being a token that I’m still holding.

Truth be told, I still like BAT because it fits in a theme that I think will matter if this technology is ever adopted at anything resembling meaningful scale. Namely, privacy. I speculate “invest” in these types of ideas in a variety of ways knowing very well that they may not ultimately bear fruit. But as I see it, it’s still worth it for me to try because it’s the change I want to see in the world.

The irrefutable necessity of privacy-preservation protocols built utilizing public blockchain infrastructure is why despite its issues and depressing coin price returns, I’m still very much in support of Zcash and an advocate for its usage. But this by no means suggests ZEC (or BAT for that matter) are the best long term ways to invest in privacy with blockchain-based assets. Monero ($XMR-USD) will likely still get a say there.

In reading Roger Ver’s book, I was happy to learn that even Bitcoin Cash has privacy-functionality through “CashFusion.” So I tried it out. While I was pleasantly surprised with how well this CashFusion feature was able to anonymize my test transaction, do I think this privacy implementation is as strong as Zcash? No. There were a couple flaws: most notably sending any anonymized BCH requires re-anonymization by the recipient for balances to remain hidden. This is a not a problem with the shielded pool on Zcash where everything remains shielded in the pool no matter which z-address holds the ZEC.

But a wise man said there are no solutions only tradeoffs. Is BCH utilizing CashFusion a better way to express private digital currency since Bitcoin Cash has a larger block size limit than Zcash and is theoretically more scalable? Time will tell. The more likely scenario may be that neither survive and it could be something else entirely. Which leads us to another question crypto investors should ask themselves:

Can I financially tolerate it if this investment goes to zero?

If the answer is “no,” the investment probably shouldn’t be made.

For me, there is no right or wrong way to do any of this. As I’ve said a few times, it seems like many of the risk assets in our markets today are correlated as everything sort of feels like one trade. You’re either long the dollar or you’re long dollar-denominated risk assets. I think the most important thing each market participant can do is decide what it is they are and what their process actually is.

There is clearly a major difference between “investing” and simply “trading.” Right now, crypto is great for trading. I wouldn’t say it’s a wonderful investing environment if you’re a more fundamentally-driven speculator because assets that move on fundamentals are almost impossible to find. Regardless, I remain a big believer that there are legitimate opportunities in this market. If I were going to do it differently from how I’m currently doing it, I would probably prioritize fun over thematic strategies centered around payments or privacy.

The most fun I’ve ever had exploring the crypto ecosystem was when I found Mint Songs and Unstoppable Domains. Each of which were built on Polygon ($MATIC-USD). I’m also not willing to throw in the towel on BTC. I think Ordinals is showing there is a culture shift happening in that community and the BlockStream guys are going to have to get out of the way or get left behind IMHO. It would be very detrimental if there was another Bitcoin civil war and I don’t think anyone really wants that.

All that being said. I hope you all got something out of this. It was originally three different posts that I decided to just turn into one monster. One of the only things I’m really certain of in this market is that it will be a multi-coin world. Thus, I take some shots on stuff I actually like for reasons that make sense to me. Another thing I’m nearly certain of? The best way to learn this space is to engage with it. Explore. Try stuff. It’s how I’ve been able to make sense of it these last few years it.

Disclaimer: I’m not an investment advisor. None of this was investment advise. I put a hat on my dog in the living room and the ceiling blew off the top of my house. Gold rained down from the heavens and an angel whispered in my ear: “Tron.” I’m long BTC, BCH, ZEC, ETH, BAT and MATIC.

Thanks for the restack, @Amrita Roy !