It Is Whatever You Want It To Be

Bitcoin ETFs are here. With eyes on capital flow, a very important philosophical question must be addressed; is this really what we want out of Bitcoin?

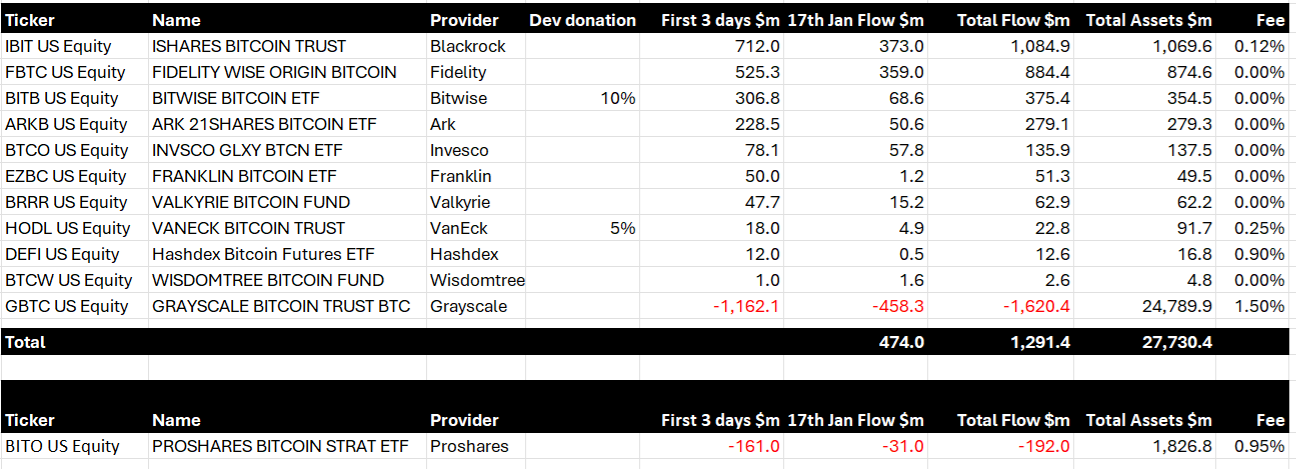

With Bitcoin ($BTC-USD) ETF approvals behind us, eyes now turn to fund flows. For this, I often look to CoinShares which produces a weekly report showing net asset flow for crypto-themed investments.

It’s probably not a huge shocker, but there was quite a bit of crypto asset flows last week following the SEC approval of 11 spot Bitcoin ETFs. With $1.18 billion in net fund flows last week and $1.34 billion YTD net flows, crypto investment capital is already equal to 60% of the of the entire 2023 net flow of $2.2 billion through just 2 weeks in January.

Side bar: I detailed why the spot ETF is different from futures ETFs in a prior post and you can read that one below if you missed it:

Now, as awesome as that first week of spot ETFs was for fund flow, where we ultimately end up is anyone’s guess. The elephant in the room is the preposterous 1.5% management fee for the Grayscale Bitcoin Trust ETF GBTC 0.00%↑.

Grayscale has the worst fee rate by far and the most to lose from an AUM standpoint. The company has roughly $35 billion in assets under management. Of which, $24.8 billion of it is in GBTC. Given these ETFs are redeemable, there is justified concern that Grayscale will see redemptions erode AUM as holders look to move funds to competitors with lower fees - of which, literally every single one of them would theoretically be in play.

On net, we want to see asset outflow from Grayscale be significantly smaller than the inflow experienced by other asset managers for our BTC “bags” to pump. Otherwise, we’re just rearranging deck chairs. That said, even if BTC moves from a high fee fund to low fee funds, it’s presumably an overall benefit to Bitcoin’s price provided the lower fee fund assets aren’t being lent out in some way. $24.7 billion GBTC at a 1.5% fee equals $372 million in 2024 sell pressure if Grayscale liquidates the management fee to pay themselves. Certainly not terrible but it would be better if these fees weren’t so large.

Side bar: I do have a personal favorite Bitcoin ETF. See which one and why:

Of course, high to low fee rotation is not a win. The promise from spot Bitcoin ETF approvals is capital inflow. We’ve long been inundated with the hypotheticals that go something like this:

There is X-trillion in AUM with company 1 and Y-trillion in AUM with company 2. If just 1% of the assets under management from those companies flow to these Bitcoin ETFs, then its banana o’clock and Bitcoin is worth a bajillion monopoly dollars.

All that stuff is fun to think about but there’s an opposing perspective that these spot Bitcoin ETFs open up cryptocurrency advocates to that goes something like this:

Why does anti-establishment currency need the state to succeed? After all, if Bitcoin is to be the new anti-fiat system, why is it apparently so reliant on that same fiat system for capital inflow?

Freedom Fighters Wear Suits?

Ahhhh, a criticism that is equal parts stale and intellectually interesting. Though not quite the “gotcha” crypto-haters think it is, it’s a valid point. Why do so many laser-eyed Bitcoiners seem to be so excited about BlackRock’s BLK 0.00%↑ tentacles reaching out for their sats? Is it a good thing that VanEck is planning to financially influence support Bitcoin developers? These are valid questions.

It's important that we understand the intended purpose of bitcoin was to eliminate the need for financial custodians. Needless to say, the rise of custodial bitcoin ownership can be seen throughout the cryptocurrency space. Coinbase COIN 0.00%↑, Grayscale, Osprey, and dozens of other entities demand a layer of trust from bitcoin holders that wasn't intended by the creator (or creators). This has happened for a few reasons, but one of the big ones would be that miner fees have made true peer-to-peer transacting on the network cost prohibitive for low value transactions. - My June 2021 article

What I do know is Bitcoin was created to be peer to peer money. If it’s sitting in an ETF controlled by BlackRock, it’s not really functioning as designed. This is not a new criticism and I’ve lamented this failure for literally years. I wouldn’t say I’m as defeated by this as Ben Hunt seems to be, but I do think his concerns are well articulated:

what made Bitcoin special in the first place is nearly lost, and what remains is a false and constructed narrative that exists in service to Wall Street and Washington rather than in resistance. - Ben Hunt, via In Praise of Bitcoin

I have felt that this is the most fair critique of Bitcoin but where I’ll slightly push back is here; Bitcoin can enjoy the benefits of TradFi adoption and still serve a purpose. I think it is still resistance in the same way that Gold (XAU-USD) or Silver (XAG-USD) are resistance. Each of which are Constitutional money even though we don’t currently use the metals for that purpose at any observable scale.

The reason I have steadfastly held firm on “bullish Bitcoin” despite its faults is the same reason I’ve steadfastly held firm on bullish Gold despite some of its faults; neither are state-issued or managed. Though you can lend against them and create as many IOUs as you soul desires, at the end of the day Jerome Powell can’t push a button and create more of either.

The enemy of my enemy is my friend.

The more people wising up to the fiat/debt servitude grift the better. If that means getting exposure through simple to buy instruments like ETFs, so be it. It is irrational to assume everyone will have both the desire and the technological competence to self-custody. And frankly, as Bitcoin becomes more expensive to use on the base layer, it might not actually be prudent to suggest everyone put their 0.001 BTC in a base layer self custody wallet or even in a Lightning wallet.

Of the 51.7 million non-zero wallet addresses holding BTC on the public ledger, 27.8 million are between 0-0.001 BTC. This is a problem if fees stay high. And at some point fees will be the only incentive mechanism for Bitcoin miners since the coin has a fixed supply and coded declines in issuance every four years (block reward halvings). But this is getting slightly off topic. I don’t think anything illustrates Bitcoin’s failure as a peer to peer money system quite like the active address ratio:

This is the percentage of wallet addresses with balances that are using the ledger on a day to day basis. Between 2012 and 2016, the average active address ratio for that entire 4-year cycle was 7.1%. Then the block space war happened. From 2017 through today the average active address ratio has been 2.3%. For all intents and purposes BTC stopped being peer to peer currency after the Bitcoin Cash ($BCH-USD) fork. BTC became “digital gold” instead.

Compare this with fellow Bitcoin-fork and perpetually despised P2P payment competitor Litecoin ($LTC-USD):

Here, we see big surges in usage and times of lower usage. During the full year 2021, the average active address ratio for Litecoin was 9.6%. So far this year the average is 10.1% - small sample size, I know. Since 2017, the average ratio has been 5%. There is just no question LTC has been better than BTC as a peer to peer money exchange vector for several years. I’m not sharing this to be polarizing or to “pump by bags.”

What I am doing is making the argument that Bitcoin isn’t everything to everyone and that’s totally okay.

What is Bitcoin Then?

the lens to view the ETF through depends entirely on what you actually want Bitcoin to be. If you want Bitcoin to be “Digital Gold” and simply benefit from ‘number go up’ as the dollar inflates away, this is great news. If you’re a self-custody maxi who wants BTC to actually be used as borderless settlement layer, this is probably less exciting. - June 2023

I’ve been working with this theory that Bitcoin is essentially just an idea. So far BTC is the most popular expression of that idea. Is it currency? Only if you have enough of it and can pay the toll. Others say it’s digital gold. Meh, PAXG is digital gold. Ben Hunt calls it “art.” Maybe. There’s actually art stored on the Bitcoin block space after all. With the emergence of Ordinals, one could perhaps argue Bitcoin is also a decentralized storage network.

The point is, we’re 15 years into the existence of this network and I don’t think we’re close to a definitive consensus on what Bitcoin actually is. Maybe where we can agree is here; Bitcoin is a globally distributed ledger system that can’t be tampered with by state regimes or individual actors. This system has a native unit of account that doesn’t require collateral backing.

Given that, Bitcoin in self-custody is not the same as Bitcoin in an ETF. You don’t actually have control of Bitcoin in an ETF. It isn’t yours, you just have a claim on it. You can’t use it if you need to in an emergency. You’re at the mercy of market hours if you want to liquidate. If you understand these differences, congrats, you are way ahead of most people.

When the truckers in Canada had their bank accounts frozen, they could use physical cash in their pockets with each other and with local merchants, but they couldn’t draw from their bank deposits. These are the environments Bitcoin is quite literally made for. Bitcoin was made for the trucker protests in Canada. It was made for the Cyprus bank bail-ins in 2013. To be sure, BlackRock, VanEck, and Fidelity buying up BTC makes it less usable as P2P cash system.

But that fight was already lost in 2017.

You’re the smartest guy I ever met, and you’re too stupid to see he made up his mind ten minutes ago. - Hank Schrader

What if Bitcoin is simply an idea and nothing more?

The idea that we have the ability to create something and distribute it globally without permission from wannabe kings or queens. The idea that we know the government doesn’t like this ability and we simply don’t care because we are in charge of our own lives. The idea that a currency can be borderless and ruled by code rather than coded to rule.

How much is this idea worth?

I would argue it’s priceless.

We Still Have So Far To Go

And I would also argue we’re not even close to where this idea is going to ultimately take us. We still don’t know how many of the ledgers spawned by this idea will remain economically viable to secure. But I’m convinced the number won’t be zero. Does this idea require the old system to succeed? Of course not. It never has and never will. The old system can participate, but it isn’t providing permission.

Because that’s what is really at the core of all of this. You need permission for a bank account. You need permission to deposit your cash. You need permission to take it back out. We have taken for granted how easy this process is for most people in the western world. But it’s not this easy for everyone. And if you do or say the kinds of things that may upset whichever regime is in control of the official printing press at any point in time, it may not be this easy for you in the western world either someday.

There is no such thing as perfection. Everything has tradeoffs. There are people, perhaps even a few of you who subscribe to this publication, who aren’t going to like this. That’s fine. One thing I have been very clear about over the last several years is I don’t worship at the altar of Satoshi.

Bitcoin is not money in 2024.

There I said it. The scaling solutions for the base layer are woefully cumbersome at this point in time. That might change and I really hope it does. But currently, today, as I write this, Bitcoin is not money. It is an idea and a really good one. It’s worth protecting. How you choose to do that is entirely up to you. And that’s really the whole point of all of this. Nobody gets to, or should get to, pick for you.

Gold? Bitcoin? Silver? Litecoin?

Why not all of it? When you get beyond the surface level stuff, it’s all really an expression of the same idea.

Disclaimer: I’m not an investment advisor. I have positions in BTC, LTC, BCH, XAU, and XAG.

Just brilliant, Mike. Brilliant. And that “mic drop” chart of an ending...