Mid-Week Portfolio Update

Mid-Week Portfolio Update

Bonds, CPI, Oil, and Metals. Let's see what Madam Ruby sees.

Before I get into this, apologies for missing the weekly subscriber-only update last week. I was traveling all day Friday, all day Sunday, and had family commitments both Saturday and for much of Monday. I figured I’d just wait until after the CPI print and the market reaction to said CPI print to dive in on some general market thoughts.

Rates, Inflation, & Layoffs

From a portfolio perspective, the biggest move I’ve made since the last update has been trading out of the short term treasury ETF SPTS 0.00%↑ - the key driver behind that decision is simply the charts.

Chart above is the 2 year treasury note. If this were a stock, this is a breakout that I’d probably consider buying. The problem is this would actually hurt the price of SPTS because the value of the shares is an inverse of the shorter term yields. Yield goes up, bond prices are actually going down.

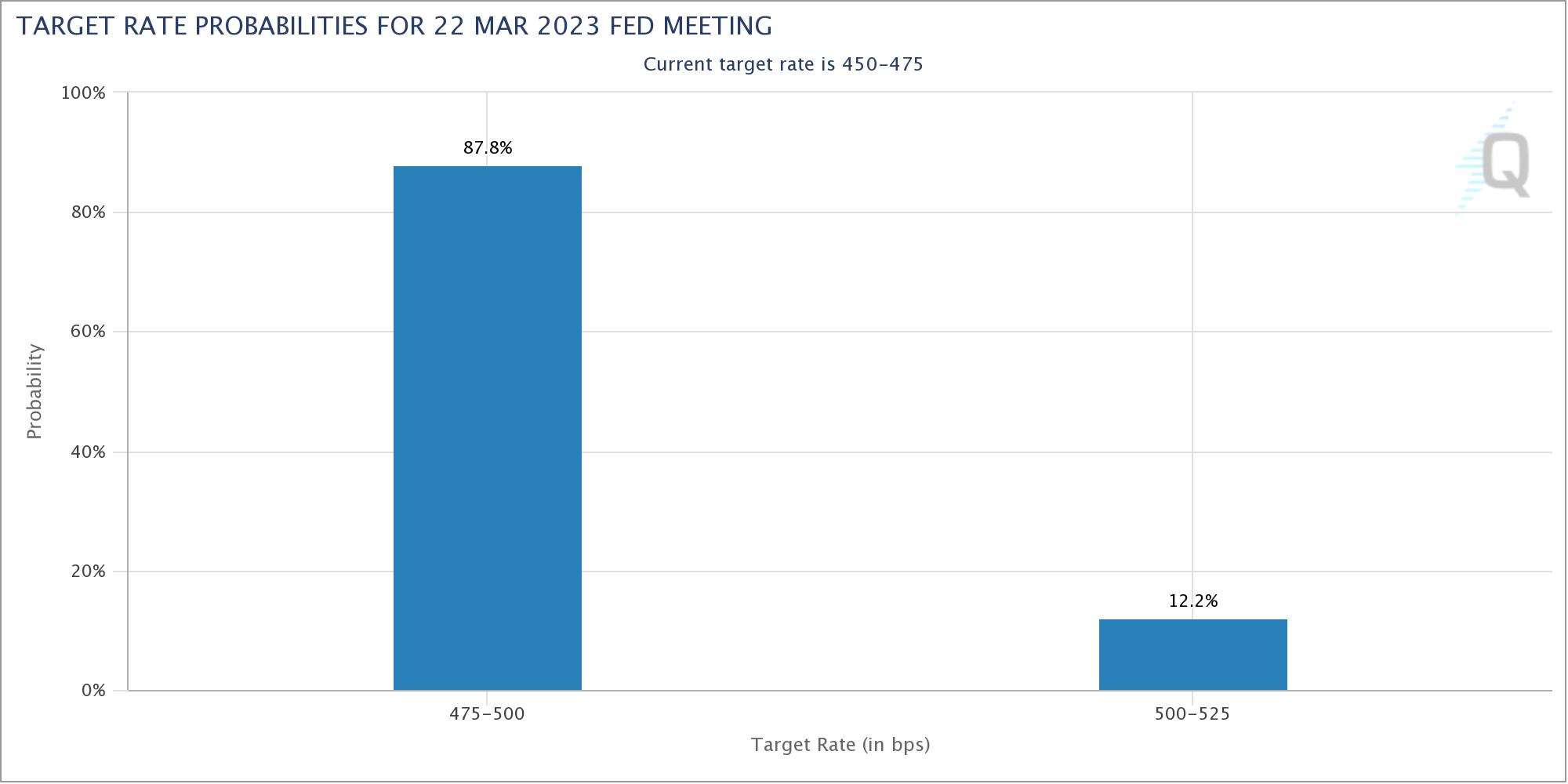

Without a Fed Pivot, it’s difficult for me to imagine US treasuries catching a serious bid. And while we’re talking rates, the CPI is still an incomprehensibly high 6.5% year over year - which while down mo/mo, is actually hotter than the consensus estimate of 6.2%. Market reaction has been a small but noticeable uptick in the expectation for 50 bps in March from 9.2% last week to 12.2% following the CPI print.

The problem for the Fed is one that I feel like I’ve detailed numerous times in the past; if the central bank has a dual mandate of stable prices and full employment, then the Fed is trapped if it has to fight persistent inflation while layoffs simultaneously ramp up.

Tech isn’t necessarily indicative of the entire labor market but the number of employees that have been laid off in tech has increased for 5 consecutive quarters and we’re only halfway through Q1 2023. The 517k jobs added surprise last week is a bit misleading because it’s an adjusted number. In reality, there were actually 2.5 million jobs lost from December to January but the expectation was for more than that. It’s a bit like suggesting not increasing the federal budget is synonymous with budget cuts; preposterous.

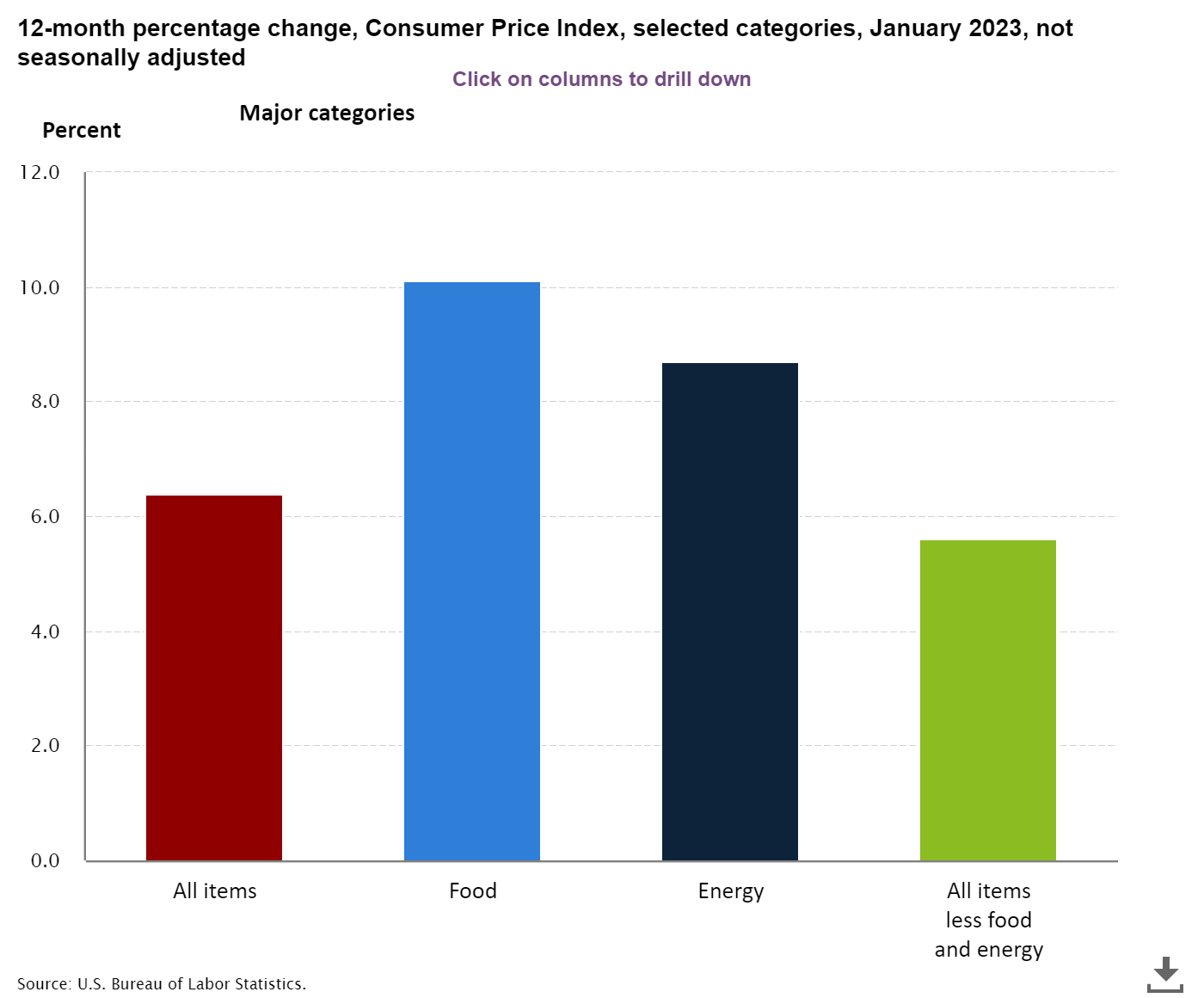

What is more likely is people who are already in the labor market are simply working harder to get by. These wonky numbers are likely irrelevant to the real people on the ground. And what “Joe Sixpack” is actually dealing with according to the BLS is a 10.1% year over year increase in food and an 8.7% increase in energy in January; two of the most important things people need to survive are still outpacing the headline CPI number significantly. Color me shocked. The overall point of this section is that stagflation is the worst hand the Fed could be dealt yet it looks like it’s possibly exactly what Powell is holding.

Keep reading with a 7-day free trial

Subscribe to Heretic Speculator to keep reading this post and get 7 days of free access to the full post archives.