The Student Debt Debacle

The student debt outstanding is now a hair under $1.7 trillion. This is a look at key reasons the crisis got so out of hand and what I'd do to fix it.

Recently, president-elect (I think?) Joe Biden was asked if there is a plan to tackle student debt forgiveness early in his presidency. He acknowledged that attacking the student debt crisis is indeed on the table and various dollar figures have been thrown out. In case you haven't seen the latest figures, we are now just $34,000,000 away from $1,700,000,000,000. Soooo many zeroes. This dollar figure is largely beyond human comprehension. But that's precisely why I didn't want to just type the word "trillion." There is no realistic way this debt is going to be paid. It's important that we understand that. So, what do we do?

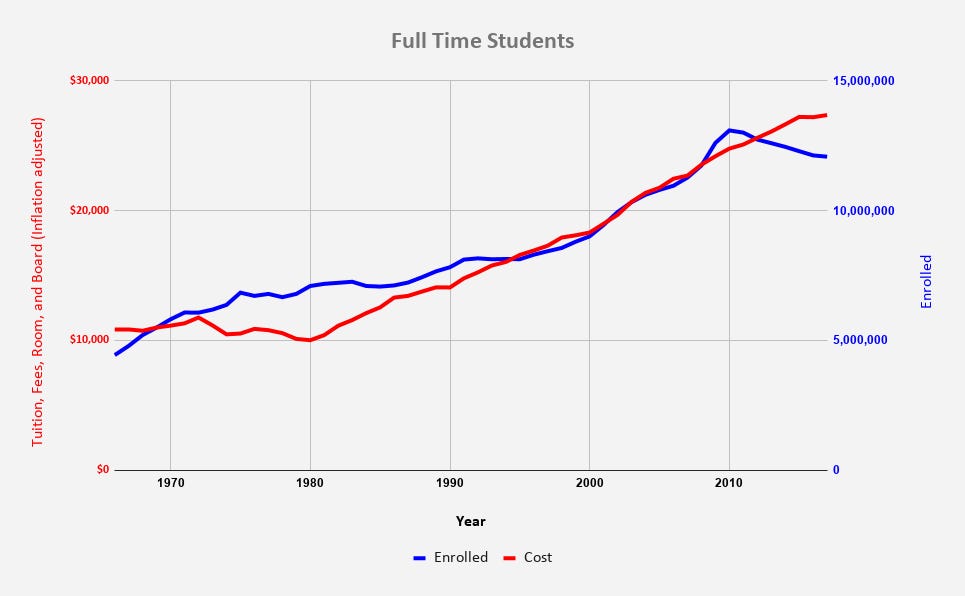

This is an incredibly complex issue and a great first step could simply be to try our best at understanding how this problem has gotten so out of control. A good starting point is looking at long term trends of enrollment vs all-in costs of going to college. This is a chart of that data for the last 55 years.

That time period from the mid-80s through the financial crisis appears as you would imagine it to, in my estimation. With an increased demand for education, price increased as well. This is because with more students, you need more teachers, more infrastructure, more books/resources, you get the idea. We can see an acceleration to a peak during the financial crisis. This enrollment inflow, at least to some degree, is likely a product of the general "there are no jobs, let's just go back to school" sentiment from young people during the recession.

But that was it. Peak full time enrollment was in 2010. Full time student enrollment has gone down almost every year since. And yet, despite the declines in enrollment, tuition costs have defied the laws of economics and continued to increase despite less demand. How could this be? Here's something to consider:

Essentially, 2010 marked the end of third party higher education lending. The federal government officially became the direct lender with the signing of the Health Care and Education Reconciliation Act of 2010. I could pick on Maxine Waters for seemingly being unaware of how student loans work, but it's too easy and I'll try to keep this article classy. I shared the video because it illustrates an important point; the people who many are looking to for a fix don't even understand the problem. Uncle Sam had already been backstopping third party loans going back to the 60's. The removal of the middleman in 2010 allowed the government to start profiting from the credit spread that had been previously absorbed by bank lenders. I've covered credit spreads here before. Essentially, the Education Department borrows the money from the US Treasury and then re-lends it to students at a higher rate. The government keeps the spread. You see where this is going, right? The government has a financial interest in children borrowing money.

I want to be clear, this is not an article that aims to put the entirety of the student debt crisis on the government. Though government involvement almost always makes a product or service more expensive and there is plenty of blame for Uncle Sam because of that, the student debt debacle is bit more complex than just one catalyst. In addition to the trajectory divergence between costs and enrollment that has taken place in the last decade, there's another point on the previous chart to consider. What the hell happened in 1980? That was the bottom for inflation adjusted tuition prices. What changed? Cost of credit changed.

I don't think it's a coincidence that nearly every cycle peak in the Fed Funds rate coincided with year over year decreases in tuition cost (65-79) or a slowing of price increases (80-present). I personally can't look at this overlay and come to any conclusion other than 40 years of ever more dovish monetary policy has resulted in higher education cost inflation. It seems we have kind of a perfect storm of events that have led to where we are now.

Lenders and the federal government have spent the last 50+ years giving teenagers who didn't know better unsecured loans to finance degrees they may not have actually needed. Lending has been made easy thanks to cheap credit from the federal reserve. Too many borrowers were convinced by parents, institutions, and prospective employers they needed college to succeed. The higher education establishment deserves a lot of blame as well. If private banks are the ones who really print dollars using federal reserve collateral that can't actually be withdrawn, then colleges and universities are the ones who have been essentially printing this student debt. Rhetoric, feelings, and good intentions can only get you so far. The proof is ultimately in the pudding. The US higher education and government loan apparatuses have had carte blanche the last few decades on student loans. The result is a lot of debt serfs working a lot of jobs they could have probably got without the debt.

That is where it gets really depressing. A recent study by TD Ameritrade found that 49% of young millennials said their college degree was "very or somewhat unimportant" for their current line of work. For Gen Z, it was even higher. That’s a staggering statistic when you consider just how indebted young Americans are with student loans. The student debt delinquency rate is 7 times higher than credit card delinquency. Maybe worse, only 24% of FSA borrowers are even paying off the principal balance. There are about 45 million Americans with outstanding student loan debt. Over $600 billion of the $1.7 trillion in student debt is with borrowers 34 years old and younger. If TD’s survey is accurate, and half of those millennials don't even need their degrees, over $300 billion of that debt has been completely wasted. To be frank, I'd wager it's actually far higher than that. And that brings us to the debt holders themselves. They are the ones who put the pen to the paper without thinking or doing any kind of return on investment analysis. Yes, many of them were duped by predatory lenders, but they are ultimately the ones who got themselves into this mess. Now that I have whipped everyone's asses, let's talk solutions.

Student loan debt is equivalent to about a third of the federal budget. The borrowers simply can’t pay it. And about 20% of the debt outstanding is essentially wealth that has been siphoned away from kids who were pushed into something they didn't understand. For context, the money wasted on useless degrees is about 4 times the high-end damages estimate for Bernie Madoff’s Ponzi scheme. And he was thrown in the clink. So it's no wonder people saddled with this debt want it wiped out.

As I type this, social media is going bananas over the very notion of debt forgiveness and as you might expect we generally have two competing takes from younger Americans. The first group falls into the "hell yes" camp - these are largely the people with 10's if not 100's of thousands of dollars in student loan debt outstanding. The second group falls into the "EFF that" camp - these are people who either didn't take on debt to go to college or who have paid off their loans through some sort of personal austerity measures. On a recent episode of my podcast, I hinted at empathy toward both sides of this argument. I will now get into this a bit more.

To do my best to make an analogy, let's pretend we're talking about automotive debt rather than student loan debt for a moment. In my money tip this week, I created a fictitious character named Stewart. We're going to use him again. And we're going to bring in Henry. If you recall, Stewart is 35, works for a living, and no longer pays someone to prepare his coffee every morning after discovering time travel and compounding growth. What you don't yet know about Stewart is he bought a brand new GMC Sierra for 64 grand financed over 7 years. Stewart essentially just took on a second mortgage. His buddy Henry works in the same building, makes a little bit less, and lives far enough away that commuting together isn't possible. Even though Henry would absolutely love a new Sierra, he knows he can't afford one and continues to drive his 2004 Chevy Tahoe that he owns outright. I'd like you to now imagine that you're Henry and you just found out Stewart's lender is going to forgive his debt obligation and let Stewart keep the Sierra too. Do you kind of feel like a sucker for sticking with the Tahoe? This is how many people who paid down their student debt feel and I think if we're being intellectually honest with ourselves, it should be easy to understand why.

So what can realistically be done? We have a situation where 10's of millions of Americans are hindered by crippling debt. Delinquencies are high, unemployment is as well, and whether they agreed to it or not, taxpayers are on the hook for all of it. Have I mentioned yet I'm glad I'm not the one who has to make these policies? But, I'm here to help so let's take a stab at it. Judging from what I believe to be the biggest catalysts in the student debt debacle, I'm going to give my plan for fixing it. It's a four-step plan.

Step 1: The Federal Government's student loan making days are over. Don't worry, our children will be fine. There is massive disruption happening in our economy and higher education is near the top of the list. I won't get into the details here, but you can use your imagination. Now that we've turned off the bad loan spigot what do we do with the debt outstanding?

Step 2: Write it off. Take the loss, taxpayers. The schools and teachers have already been paid. Unlike mortgages or automobiles, there isn't any collateral that can be repossessed for liquidation in a bankruptcy. It is a total lost cause. Just eat it. Don't worry though, I have some goodies for you too, taxpayer.

Step 3: Currency drop. There is also something in it for Henry and his Tahoe. Each non-student debt holding adult citizen in America will get a one-time cash infusion of $20,000 directly to their bank account. Just like we did with the stimulus this year. That figure, while seemingly massive is half the average student debt outstanding per borrower. In addition to that, I'm adding $300 billion for adults who hold less than $20,000 in student debt. After having their debt wiped out, they can apply for a "fractional drop." An example of how this would work would be if Henry has $15,000 in student debt outstanding, his debt will be wiped and he can apply to receive a fractional drop of $5,000 to equal the $20,000 benefit that non-debt holders will receive. This massive money drop comes out to about $4.5 trillion when we deduct kids and student debt holders from the US population who would be eligible to receive it.

Step 4: Credit is too cheap. If the cost vs enrollment chart tricked you into believing higher education prices have been driven by demand. Apologies. That's just part of it. That demand has been stimulated largely by government policy and cheap credit. We need capital costs to actually be allowed to have price discovery. This should really be step 1, but hey, I'm trying to be realistic.

In total, when you factor in the $1.7 trillion in student debt write off, this amounts to a $6.2 trillion dollar stimulus bill. That figure would have seemed asinine to me 12 months ago, but we're now in the age of money printer go brrr. What's the use of having a money printer if it can't go brrr? This plan is simple. Straight liquidity and debt relief for people and nothing more. No strings attached. No special allowances. No BS hidden in the bill. It should be one page long. You may be asking, why do this? Why give money to people who don't have student debt as part of this? All of this monetary policy is going to come home to roost through significant currency devaluation. That hurts savers and retirees far more than it hurts debtors. Savers, people on social security, and labor force participants who chose not to go to college need to get something out of this deal. It should help all Americans pay down debt. Mortgage. Auto. Credit card. There's a ton of it. Everyone wins. Kinda.

That's my take on the student loan crisis. The debt is an absolute disaster. There is virtually no chance it can possibly be paid properly. There are a ton of factors that have played into what caused it. And the most logical way out in my mind is essentially a soft debt jubilee. I'm never going to please everyone with this plan. And that's entirely okay. It's just my read on the situation and what I'd push for if I was in congress.