Where Were The Signs?

"Then put your little hand in mine, there ain't no hill or mountain we can't climb."

Well, it’s Groundhog Day. Again. - Phil Connors

Roaring Kitty is back… again. Ed Yardeni thinks we’re at the beginning of a bull market… again. And NVDA is up 5% in a day where it makes yet another new all time high because… I’m not really sure why to be honest. Perhaps stock splits are viewed as fundamental catalysts… again.

At this rate, it’s just a matter of time before NVIDIA NVDA 0.00%↑ is the largest company on the face of the earth by market capitalization despite generating a small fraction of the revenue each of these other behemoths have brought to the table for years, let alone one year.

Is this warranted? I obviously don’t think so. But we can’t argue with NVIDIA’s gross margins (currently) and I suppose every mania gets its Cisco Systems CSCO 0.00%↑- which, by the way, appears to be exhibiting one of the more textbook head and shoulders patterns I can recall seeing in the wild:

To be clear; I hold absolutely zero ill will to those who keep booking stacks in this market - many of you are my readers and I’d laugh about it with you over a mug of suds anytime. We’re all traders whether we realize it or not. I’m not irritated with the players, it’s the game itself that bothers me. But get your paper and don’t apologize for it. Just remember, value is subjective and the incremental buyer may not emerge at the exit price we might want.

Maybe it’s that I’m a contrarian to a fault. Maybe it’s that I’m too much of a degenerate gambler to quietly ride a wave. Maybe it’s that I just don’t want the equity market to keep going up in spite of economic data that is clearly showing consumer deterioration. Whatever the reason, bonds are actually starting to look interesting to me with equities again at all time highs. Look, I get it. This is the Heretic Speculator blog. We’re generally more interested in counter-system assets like metal or Bitcoin. But hear me out…

The Case for Bonds

I’ve mentioned the iShares 20+ Year Treasury ETF TLT 0.00%↑ in the past and have traded in and out of it a few times (I’m actually long at the moment with a sub-$91 average). Those positions have been a small fraction of what I have had allocated to T-bill funds like WisdomTree Floating Rate Treasury ETF USFR 0.00%↑ or Fidelity money market funds over the last 12 months. The later of which is basically a cash equivalent that pays me to do nothing and has the backing of short duration T-bills that are no longer than 6 months to maturity.

As beautifully as the ‘T-bill and chill’ strategy has worked for those who want no part of chasing unicorns or the index, this approach has indeed underperformed the “riskier” equity market. Everyone’s strategy is different. And the problem with ‘T-bill and chill’ is that if rates start dropping substantially, the risk-free rate strategy stops working somewhat quickly.

But if we hold the view that rates will indeed come down - and they probably have to or risk of hyperinflating the currency grows - is there logic in trying to lock in some of these debt yields for a longer period of time? The answer likely boils down to where you fall on equities and where you fall on inflation. If you think the official rate of inflation is going back up to 10%, this idea may be an avoid. Additionally, if you think we’re at the beginning of a melt-up in stocks, then this trade probably isn’t for you.

However, if you think we’ve already been in the melt-up for the last decade or so and believe this thing could fall apart at any moment when everyone realizes we can’t all get the same exit price when boomers turn into forced 401k sellers, then a “risk-free” rate of 4.8% might make some sense. Of course, “risk-free” is in quotes for a reason. Investments without risk do not exist. Period. When holding bonds directly, there is inflation risk and duration risk. Hard default risk? Probably not with a magic money printer. Soft default through currency debasement? Absolutely.

If you buy a 10-year bond that yields 4% and inflation surges back above 5%, you’re getting a negative real yield. If you buy a 10-year bond at 5% and interest rates on the 10-year rip up over 6% to combat that 5% inflation, you have to hold the bonds to maturity or you’re selling at a loss. This is less of a problem if you’re an individual buyer deploying your own capital. It’s a much bigger issue if you’re a money manager or bank and you get a request for withdrawal. Regardless, neither of your options are great. You’re either selling the bond at a loss or you’re holding an asset to maturity that you know is losing against inflation in the long term. Those are the risks with bonds in a nutshell.

The question then is which bond can we even justify buying if we think rates are going to go down even if just temporarily? The 20 year? I wouldn’t touch it, frankly. Playing around with TLT for price appreciation is fine, but I suspect purchasing power erodes dramatically over the length of the arrangement if you’re owning these things directly. That’s not what I’m saying here.

Allow me to briefly make the case for the US 2-year bond. Or, for the trader, the iShares 1-3 Year Treasury Bond ETF SHY 0.00%↑. A weighted average maturity of 2 years and an average yield to maturity of 4.81%. When bond yields inevitably start going back down, SHY holders will keep those ‘T-bill and chill’-like returns while the shorter duration debt yields roll over. Also consider that at 4.8%, the yield on 2-year treasuries is still higher than the yield on both the 10-year and the 20-year bonds:

This is really just expressing the inversion of the yield curve in a different way. Remember that yields must be viewed counter-intuitively. When yields on bonds are declining, it’s because those bonds are rallying. The more demand for the perceived safety of bonds, the lower the rate of interest the bond issuer needs to offer.

Generally speaking, the longer you’re willing to delay gratification from spending and loan your capital to the government so it can spend it on blowing people up, Egyptian tourism, Monkey casinos, and PPP loans given to literal toy dolls, the better the yield on that loan should be. Thus, it’s indicative of a problem in the market when the yield on the 10-year minus the 2-year is negative. And this is exactly what we’ve had for nearly two full years:

At some point, this is going to have to end. But in order for that to happen, there has to be an incentive for investors to get interested in bonds again. I believe a lot of bad things about the Federal Reserve bank, but one thing I don’t believe is that Daddy Jerome wants to own all this US debt on the Fed’s balance sheet.

Thus, he needs someone else to buy Janet Yellen’s shitcoins and since foreigners aren’t nearly as interested in our Ponzi scheme as they used to be, it’s probably going to have to be the elder abuse supporters and the domestic terrorists who take on that burden.

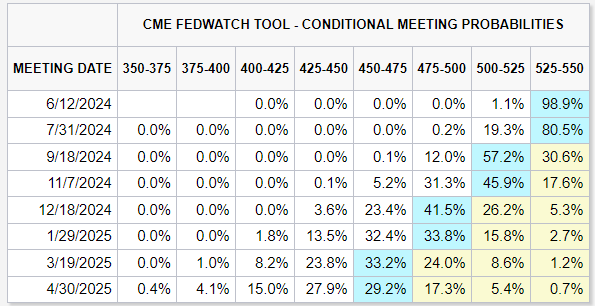

The question then is what does Powell have to do to get the market to start bidding the US 2-year? Answer: nothing. He’ll do the same thing he did on the way up… watch the market do it for him.

At one point in January 2021, the yield on the US 2-year was 11 basis points. The spread between the 2-year and the effective rate was 3 basis points. One year later, the 2-year yield hit 1%. It took 5 months for the Fed to catch up.

So that’s my argument for the US 2-year.

The Capital Flows From…

Stocks! Sorry. I’m not touching my dividend-paying value stocks. This is not capital that I’m pulling from Gold, Silver, or Bitcoin. Believe me when I say those are core long haul positions. In a way, they are very much hedges against the treasury bet that I’m now making. If I’m wrong on the 2-year bet, I believe it will be because capital is flowing instead to anti-state assets like BTC and Gold. Capital that I’ve put into SHY is mainly capital that has been in some of my smaller equity allocations.

I’m trying to skate to where I think the puck is going not where it already is. Everyone loves equities. There are numerous calls for higher yields. Particularly from very smart people like Jim Grant. But I think rates are going to go down first and I think it comes at the expense of equities.

I believe there are numerous signs that we’re in peak tech stonk mania. We’ve seen this movie before. They literally made a movie about Roaring Kitty. Hopefully the sequel is being greenlit as I type. Jensen Huang autographing a woman’s undergarment isn’t quite on the level of Mark Minervini pretending to have a technical issue when asked about a company he tried to pump on CNBC’s viewers, but it’s still a heck of a signal. As is Jim Cramer coming out on his show this evening in a leather jacket in homage to Jensen Huang.

I leave you with a portion of Cramer’s glowing ode to Jensen Huang on CNBC tonight:

I have been in awe of this man for ages. Not just because he’s a visionary businessperson, but because he happens to also be a really nice guy.

On second thought… send it to $4 trillion.

Disclaimer: I’m not an investment advisor. I’m a salty son of a gun who missed out on NVDA. I’m long Bitcoin, Gold, Silver, TLT, and SHY.

Easily one of your best, Mike. Love this one. A few thoughts:

1) you could still be early on NVDA - and correct for that matter - but at this point I’m not fighting the trend (says the guy that agrees with you!) That 10:1 forward will juice that thing like no other. And while the SP is going nuts, the CAGR on revenue and income is absolutely disgustingly awesome. Overextended? Yes. Beginning of a new tech revolution? Also yes. Have a sold a single share? Nooooooope.

2) Mugs of Suds will happen, just bring your tin foil hat.

3) “Yo, hate the player not the game” - Mike Lowry

4) you’re welcome for the boobs 😉

5) leaving the best for last here (and something I think is CRUCIAL to this article) is the fact that it’s an election year! No one will dare rattle any cages at this point. IMHO I think we’re in a “higher for longer” and while we’re starting to see cracks, I’m of the mindset that we might be closer to stagflation at this point, which would support that thesis.

6) ok, back to tacos and tequila🍸

Ghostbusters.

Dr. Peter Venkman.