Death, Taxes, Private Placements

Valuation is a funny thing. If I put $5 in a box and you can't take it out, would you pay $10 for the box? This is not a trick question.

Earlier today I dropped a fresh note on Seeking Alpha covering MicroStrategy MSTR 0.00%↑. The stock is garnering interest from the investment community today as it follows in NVIDIA’s NVDA 0.00%↑ footsteps in becoming yet another public company doing a 10-1 stock split. Given what I think can reasonably be assumed to be an attempt to generate buy interest from retail traders and investors, the reduction in the sticker price figures to bring in fresh suckers liquidity.

The fact that a stock split changes nothing about the company fundamentally or the total valuation of the equity? Irrelevant!

Not on Seeking Alpha? Here’s a freebie link for your troubles.

My take on MSTR today is pretty straightforward and its certainly not one that will be a mystery to anyone who has been reading Heretic Speculator since March. However, this new piece has the stock split angle and an updated look at the company’s equity value to it’s Bitcoin treasury. Spoiler: I still think the stock is dramatically overvalued but it could be worse…

If an 80% premium to digital asset market value is intense, what do we call 2,000%? And no, I’m not making this up. Such a product exists.

Take for instance, Grayscale’s OTC-traded Filecoin Trust $FILG. This ridiculously small, illiquid fund that holds just $5.8 million in AUM has a market valuation of $113.5 million - a full 2,000% premium to net asset value. And for the unadulterated who joined more recently and are unaware, this is a closed end fund that exists entirely to track with the price of Filecoin ($FIL-USD). That’s it. There’s nothing special about it.

There are 1.59 million shares outstanding. Each share has 0.92 FIL. The price of FIL is a little over $4. The NAV of each share is $3.87 as of market close this afternoon. Share price? $71.

Madness.

And believe it or not, this was much worse a few months ago when the same fund traded at about a 4,000% premium to NAV. But now, the fund’s premium is coming down while the price of the coin itself has fallen by more than 60% over the same timeframe. That’s a tough break for FILG bulls and it highlights the danger in one of the most interesting arbitrage trades in the markets - privately placing with Grayscale.

Private Placement Growth

Here’s the TLDR on all of Grayscale’s single asset crypto products with the exception of the Bitcoin Trust ETF GBTC 0.00%↑; these funds are closed-end, meaning there’s no redemption of the assets either in-kind or cash-settled. This is the reason GBTC’s conversion from a CEF to an ETF was so important.

When GBTC was the only game in town, it traded at silly premiums to NAV as well. During the 2017 bull run, GBTC briefly traded twice net asset value on two separate occasions. Over time, competing products came into the market and shares of mining stocks became a better way to generate degen-like alpha on Bitcoin in the public markets. During the depths of crypto winter in late 2022, the fund traded at a 50% discount. This was incredibly frustrating for shareholders because they couldn’t just redeem the BTC held in the fund to unlock shareholder value.

At that time, many of us put this trade on from the long side with the hope that either the fund’s NAV would normalize organically or it would be successfully converted to ETF to allow for asset redemptions. That trade ultimately worked beautifully and I know a few of us made a lot of money doing it. But now, we have the opposite:

With the exception of the Ethereum and Ethereum Classic funds, every single-asset altcoin fund offered by Grayscale trades at a considerable premium to NAV - even the larger ones like Litecoin and Bitcoin Cash which have AUM figures well over $100 million. But here’s the catch with these funds, even though they’re still closed end and the assets can’t be redeemed at a discount, accredited investors can put more into the funds at net asset value. This is called a “private placement.”

So for example, I see Litecoin is trading at a 200% premium to NAV through Grayscale. I decide to send Grayscale some of my LTC for inclusion in the Grayscale Litecoin Trust $LTCN fund. Grayscale takes that LTC and creates new LTCN shares with it. Even if the value of my LTC is only $25,000 - the shares that I just helped create are worth $75,000 on the open market because of the 200% premium.

The only catch? A lockup period. I have to wait a year to be able to sell my new shares on the open market. This makes private placements something of a race against time and other private placement providers. When my year is up, my hope is that the premium didn’t collapse, or worse, turn into a discount. The latter of which is literally how Three Arrows Capital blew up back in 2022 and took a bunch of other companies down with it. But I digress.

Grayscale reopened private placements earlier this year after most of the firm’s single-asset funds flipped back from discounts to enormous premiums. And we’re seeing holdings take noticeable moves upward:

Grayscale’s FIL position has increased from just 104k in March to over 1.4 million coins as of July 10th. This is a by far the biggest increase in holdings for any one fund at 1,300% - but it isn’t the only fund with large inflows:

Chainlink and Basic Attention Token are each up over 200%. On the surface, these “inflows” seem bullish. Perhaps they are for the coins themselves. But these are very bearish indications for holders of these Grayscale funds because the intention from the private placers is to deposit at NAV and liquidate at a premium. The problem is they’re not going to all be able to get out at the price they want and that will ultimately drive these premiums much lower.

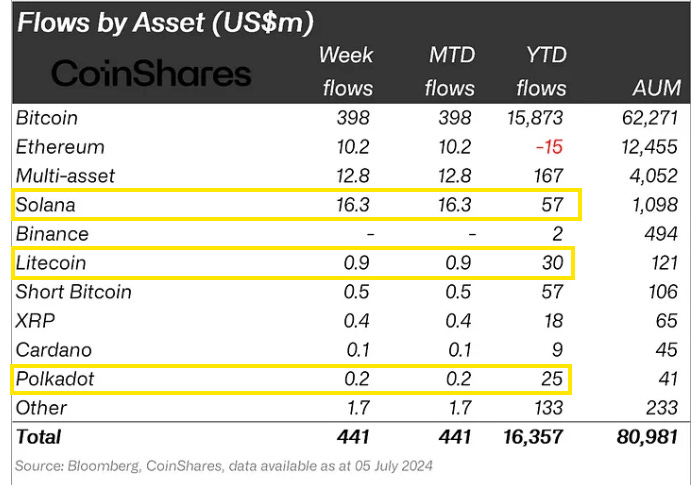

Take a look at the top 3 altcoins by YTD flows according to CoinShares last net flow report from earlier this week: Solana, Litecoin, and Polkadot.

Grayscale’s Solana fund trades at nearly a 600% premium to NAV

Osprey’s Solana fund trades at more than a 200% premium to NAV

Grayscale’s Litecoin fund trades at a 200% premium to NAV

Osprey’s Polkadot fund trades at a 70% premium to NAV

Osprey’s Polkadot fund doesn’t have a large enough AUM to account for all of that net flow, but I’m fairly certain private placements are playing a role in that investment flow. For the Grayscale funds, these private placements largely started in February and March.

Risks In The Arb

I alluded earlier to the risk in the arbitrage trade and cited the 60% decline in Filecoin. Imagine buying FIL at $11 in March for private placement with Grayscale. At the time FILG shares are $350, now they’re $71. Some of these private placers might not actually get out of this trade alive if the premium falls further in tandem with the coin.

That’s the risk. Time from lockup. The only question in my mind is how long it will take these premiums to vanish again. The idea that it will happen feels like the closest thing to a certainty in these crazy markets. But who knows?!

Disclaimer: I’m not an investment advisor. The only Grayscale fund I like at this point is GDLC. And even that is purely because of the discount rate.