The Rules of The Game

We are all just prisoners here of our own device.

So why would you save at 4%, 2%, or 3% at any bank when inflation is 8%? Or 18%? Or at Shadow Stats 9%? You’re losing money. That forces you to take more risk. Forces you into Wall Street. Wall Street forces you into the markets. Markets give you capital gains. Capital gains give the government money. It’s almost a national interest right now to be in the markets to look for yield. - Matthew Pipenburg, via Palisades Gold Radio

Last week Seeking Alpha published my latest piece on the Direxion Daily S&P 500 Bear 3x Leveraged ETF SPXS 0.00%↑. Here’s a freebie link for those of you who don’t subscribe to that platform. If you like, you can think of it like the sequel to Breaking the Index from the end of June.

Here’s my favorite chart from the SPXS piece with the accompanying commentary:

in just six months the S&P 500 has already surpassed even the most optimistic price targets for the end of 2024 from major analysts. To recap; economic data is weakening judging by consumer data and jobless claims, market breadth is abysmal, the market cap to GDP ratio is at nosebleed valuations again, every major analyst price target for 2024 has already been reached, and we're four months away from an election where we don't yet know for sure who is going to be on the ballot. All of this while bonds offer a positive real yield.

The S&P’s SPY 0.00%↑ 15% year to date rise in just 6 months has obviously pushed many of these same analysts to simply raise their end of year forecasts. Because after all, why not shoot for the sun when you’ve already hit the moon? It might kill you, but that’s a problem for another day. Taking a different approach from raising S&P forecasts, Piper Sandler is just going to stop offering price targets for the index altogether:

I didn’t see the value in raising my target again, given how it’s become such a poor form of explaining stocks, which is what it was initially meant to represent. - Michael Kantrowitz, Piper Sandler Chief Investment Strategist

One might ask, so what? The optimist assumes we can simply grow into valuations. Okay, fine. But what if the “growth” is largely, or even entirely, deficit driven?

If we take government spending trillions of dollars that don’t exist out of the equation, GDP is actually negative. Like every good story, this tale will have both a beginning and an end. Many see the problem here, the solution is much less clear.

Which Game Are We Playing?

Here’s an opinion you probably won’t find from too many other financially-focused newsletters or analysts; chasing gains in bafflingly overvalued technology stocks isn’t a great way to “invest.” Speculate, sure. But if our returns are dependent on debased dollars from a future buyer rather than from a distributed share of real earnings, we’re probably not playing the game we think we’re playing.

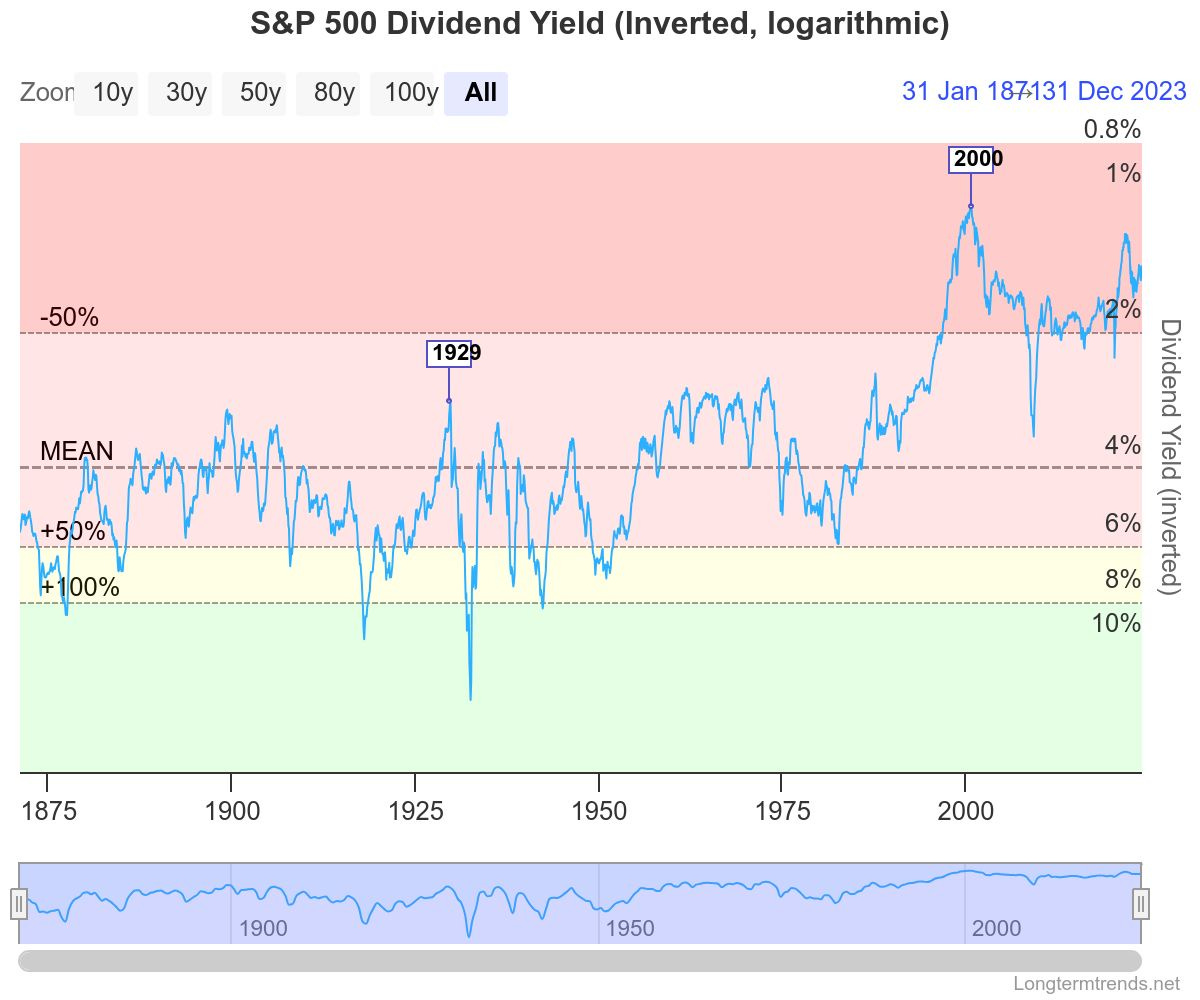

The S&P 500 rose nearly 400% from the “Roaring 20’s” lows of 1921 to the peak in 1929. Obviously the crash of 1929 happened and the index collapsed by almost 90% over the next 3 years. Fun fact: even at the 1929 peak, the index still paid a 3.1% dividend yield.

We are well below 2% today and have been for most of the last 20 years. Value has not done well against growth and that’s probably a big understatement. I think this will eventually reverse and I’m not alone in that assessment:

I have in the past written about the difference between dividends and harvested capital gains. One is a business outcome; the other is a market outcome. I’ll die on that hill. In fact, I already have. Very few people have accepted that argument. - Daniel Peris, Federated Hermes Portfolio Manager

Daniel Peris has a criminally underappreciated Substack newsletter. Perhaps because market participants don’t seem to care about dividends or value. I’m not really sure. But he practices modern investment heresy and is also a terrific writer. I like him.

Don’t get me wrong; I’m not saying short the index or even sell all your stocks. My goal here today is to merely make the argument that we should acknowledge the game we’re in if we truly want to play it to win. Most people like stocks. I get it. They’re liquid. They’re exciting. It’s easy to buy assets that are correlated to markets or products that we might individually understand well.

Like Air Jordan sneakers? Catch the knife in Nike NKE 0.00%↑.

Think crypto is here to stay? Coinbase COIN 0.00%↑ at 10x forward sales isn’t the worst valuation in the market.

Buy stuff in bulk? Costco COST 0.00%↑ only trades at 55x forward earnings.

I jest, but I hope the point landed. Nike is actually the only company mentioned above with a divi that beats the index. But there are clearly problems there. Not the least of which would be one of the most popular sneaker reviewers in the world saying the company’s products suck earlier this morning:

Let’s take it back to base assumptions for a moment. We invest capital because we’d all like to be able to build wealth and retire someday. Given this, I’d argue that we’re all essentially just risk managers. Is the primary risk we’re trying to manage not ultimately perpetual currency debasement?

If yes, then the equities and treasuries that have been the recipients of invested capital for the last several decades are brimming with counterparty risk that must also be managed. And make no mistake about it, these investment products are programmed to receive…

You can check out anytime you like. But you can never leave.

Cue the guitar solo.

Playing The Heretic’s Game

How does one hedge that counterparty risk from traditional investment products? You take delivery. And that is exactly what is happening in the yellow metal market:

Gold ETF flows have been negative since 2022, yet Gold’s price rises. Why? Because Gold is arguably one of the only investable assets that fundamentally lacks counterparty risk if you don’t want it to. Businesses can go bust. Stocks can be diluted. Brokers can go bankrupt. And debt issuers can default. But Gold in your hand is nobody’s liability but your own.

Even Bitcoin, which I still absolutely believe deserves a place in a broader portfolio, requires the ledger security provided by miners to have anything resembling utility. And BTC that is not held directly relies on additional counterparty risk. Speaking of which…

It’s time we talked about Mt. Gox.

Here’s the TLDR version:

Mt. Gox was the largest Bitcoin exchange up until its demise in 2014 and filed for bankruptcy protection. There was an apparent hacking of the exchange and roughly 850k BTC were stolen according to Mt Gox. Of that loot, a small fraction of the stolen BTC has been recovered. But at current prices, the value of the BTC originally held by the trustee is nearly $10 billion. These recovered funds are now starting to move to a handful of exchanges that have agreed to work with creditors who are going to get repayments over various schedules. Some are within 90 days and others sooner than that.

So far, the trustee has relinquished close to 50k BTC:

According to data from 21Shares, approximately 94.5k BTC have yet to leave the trustee. This means there is an additional $5.4 billion in Bitcoin that could theoretically be sold if creditors decide to liquidate upon receipt. And again, even the 50k that have already moved have not necessarily been repaid to creditors yet. This leads to the obvious question:

What are the creditors going to do when they receive their BTC?

Kneejerk reaction from many has been that the creditors will sell when they get their coins back. There’s good reason for that belief:

Bitcoin is only up about 11,000% since Mt. Gox went under. So even just $100 on Mt Gox in February 2014 when the exchange ceased operating is worth about $1.1 million today. Would you take the win?

Others have taken a more positive outlook on the Mt Gox situation and have reasoned that Mt Gox holders would have been long term holders who simply won’t sell. Frankly, I think this is wishful thinking. Complicating matters is other large market holders are also selling BTC simultaneously. Take for instance Germany:

Like many other countries (including the United States), Germany has acquired a multi-billion dollar Bitcoin position through asset seizures over the years. To it’s credit, the US Federal Government’s BTC selling over the last 18 months has been far less intense than what we’ve seen from Germany:

This is not meant as FUD. Rather, data points to help each individual make their own assessment about potential sell pressure on BTC going forward. We know Germany is liquidating. The long term position for the US isn’t as clear. As of July 9th, my bias is still for lower BTC prices shorter term.

I see a coin that is once again testing the 200 day MA and may indeed close above it today. The altcoins look much less convincing. Same story for the miners.

I don’t need a single digit crypto fear and greed reading. But this market has far more pain tolerance than the US equity market. So let’s see it…

And when that pain comes, we all know what the powers that be will do in response and which asset classes will react the strongest to that response.

Set your board. And then make your moves.

Disclaimer: I’m not an investment advisor. I like boring stocks, Bitcoin, and precious metals. Despite a tactical SPXS position, I’m selectively net long the stock market. I speculate in coins and save in Gold.

It looks like you made a good call on SPXS, a bit more than 5% gain since you published your report. Nowhere near max pain, but your reasoning appears sound. Congrats