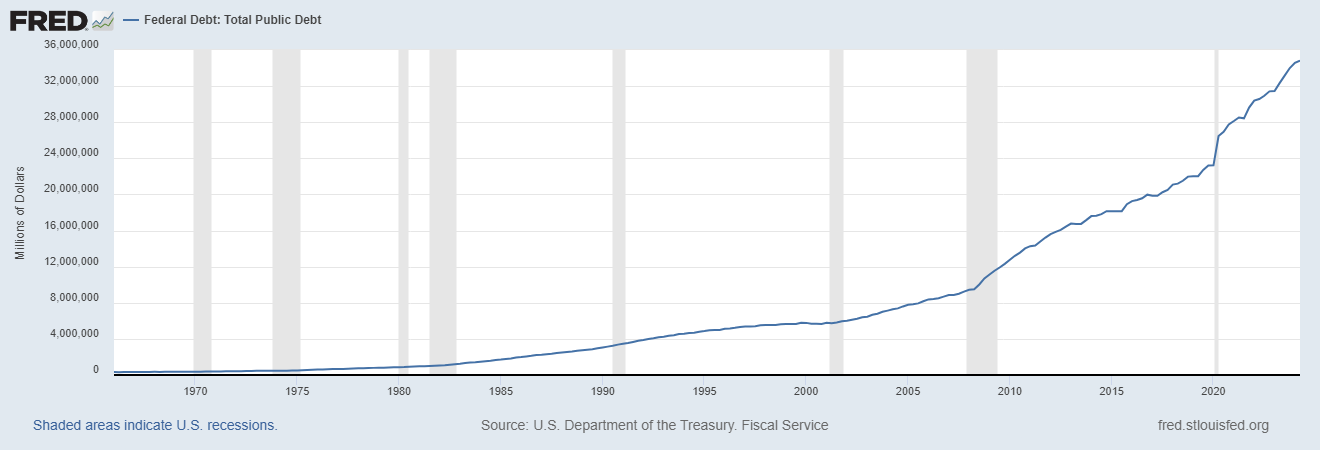

Yes, The Debt Matters

And you still don’t own enough Gold.

Our latest presidential debate came and went. With it, comes friendly banter, reactions, and hot takes. What I have found to be anecdotally true in the time since last Tuesday night is it’s easier to have an engaged conversation about Taylor Swift’s Harris endorsement than it is to have one about the national debt. Bringing up the latter results in cricket noises and/or an assertion that the country’s enormous debt load doesn’t actually matter.

Nothing could be further from the truth.

Which, I suspect, is why it is no longer a debate stage issue as neither party even acknowledges it as a matter of policy. To be sure, I blame Republicans for this. Democrats are fairly honest about their platform of feelings trumping mathematics. The elephants are supposed to know better than this yet they still behave as though they are donkeys.

But to believe the debt doesn’t matter is no different from the belief that banks didn’t fail in March 2023. It is to believe the laws of accounting have ceased to exist or that debt holders aren’t in the business of being paid back. I assure you, regardless of whether or not the human brain is capable of processing the magnitude of four commas and thirteen zeros, the debt is just as real as a home mortgage or a credit card balance. Someone owns that debt and that someone certainly expects to collect.

And while it might be easy, convenient even, to hand wave away America’s bond holders as some Milburn Pennybags lookalikes who don’t deserve to be made whole, the truth is America’s debt owner is actually the person staring you in the mirror. This is who I’m concerned for. Uncle Pennybags will be fine; he owns the rails, the utilities, and the hotels. He’s hedged with real assets. Are you?

Fractional Reserve System

Sure as you’re born, if you have a bank account with dollars in it, then you are indirectly a US debt holder. Surprise!

I assume you’d like your money back so for the remainder of this post I’ll be operating with the preconceived notion that any deposit with your bank is not a donation and is instead capital that you’d prefer to access some day. We’ve briefly covered these concepts in the past, but let’s dive into this once again.

Most banks in the US financial system are fractional reserve rather than full reserve. A full reserve bank holds depositor assets 1:1. Meaning, if Milburn deposits $1,000 with Full Reserve Bank of Monopolyland, that bank is storing the capital and Milburn can come get it back out anytime he wants. Short of the bank committing fraud, that capital will be there and ready when Milburn returns for it.

If instead Milburn deposits his $1,000 with Fractional Reserve Bank of Monopolyland, the moment he walks out the front door that bank is putting his money to work by loaning it out and earning interest income off Milburn’s capital. If the bank doesn’t totally suck, it’s potentially even paying Milburn some of the interest from those loans and keeping a portion for the bank’s shareholders.

Just about every bank operates the way Fractional Reserve Bank of Monopolyland does as described above. Although many of the ‘TBTF’ variety don’t pay depositors diddly on the loans they’re making (🚨horrible deal alert🚨), a reserve ratio of 10% isn’t historically uncommon. In our Milburn example, Fractional Reserve Bank of Monopolyland would be loaning out $900 of Milburn’s $1,000, thus, leaving $100 if the bank is practicing a 10% reserve ratio.

Where does that $900 go? A variety of places potentially. It could be a small business owner who is borrowing to expand operations. It could be a car buyer who needs financing. These are viewed as riskier because the car buyer could stop paying or the small business could go under.

The borrower who is viewed as “risk-free” is Uncle Sam. Odds are, most of Milburn’s $900 was loaned to the government through treasury bills or shorter term bonds. Hence, Milburn is now indirectly exposed to US debt. And as we’ll see in a moment, the idea that Uncle Sam’s debt carries no risk is preposterous.

What’s The Problem?

This system only works if the parties involved maintain confidence that it won’t fail. But it can fail and likely will fail because of a very important detail: Milburn’s borrowed money is ultimately spent by the borrower. Which means somebody else in the market also has a claim to the exact same dollar that started from Milburn’s original deposit. Consider:

Milburn deposits $1,000 with Fractional Bank

Fractional Bank loans $900 to the US Treasury Department in exchange for US debt notes

That $900 in US debt notes then goes to the Federal Reserve Bank

The Federal Reserve buys the US debt with $900 in new currency units created out of of thin air

The Treasury Department distributes the original $900 to other branches of government where it is spent on essential programs - and also on guys like Bob, who is studying the impact of Russian cats walking on treadmills (🚨money laundering alert🚨)

In this example, the end result is Bob and Milburn now both have a claim on the same dollars. And here’s the best part; Bob deposits that money with Fractional Reserve Bank of Monopolyland as well and this process repeats over and over again, creating new currency units from nothing every time.

So what happens when Milburn wants his money back?

A Dollar Tomorrow For a Burger Today

Now that we’ve established that most of Milburn’s initial capital has been spent on buying borrower obligations and/or government largesse, what happens when Milburn comes back for his deposit? This is where things get really fun…

Lets pretend Milburn wants to buy a Nintendo Switch for his kids for Christmas. He goes to the bank to take out the $300 needed for the purchase. Since the bank only has $100 of Milburn’s capital sitting in cash, it has to sell $270 of the debt that is currently backing most of Milburn’s initial deposit.

SIDE BAR: $270 in debt must be liquidated to keep a 10% reserve ratio… $1,000 original deposit minus $300 withdrawal equals $700 balance… requiring $70 in reserve at 10% ratio.

The bank selling $270 of that US debt to another market participant to get Milburn’s withdrawal settled usually isn’t a problem. But it can be if the value of the debt that must be liquidated moves against Fractional Reserve Bank. This is exactly what happened in March 2023 when several banks started failing because they mismanaged their debt duration profile. Banks don’t want to borrow short and lend long. Which is all the more reason why one should take the word of a central banker with an enormous grain of salt.

The Chairman of the Federal Reserve told the world the central bank wasn’t “thinking about thinking about” raising interest rates in June 2020. At that time, he told the financial markets that rates would stay at zero through 2022. Then he raised rates at the fastest pace on record by year over year change percentage beginning the first quarter of 2022. Now all of the banks that bought treasuries on his June 2020 rate guidance are underwater and need bailouts.

In most instances, Fractional Bank shouldn’t have much of a problem liquidating debt to settle withdrawals. The problem comes when everyone asks for their money at the same time. Thus, we come back to Bob. It is mathematically impossible to settle both obligations to Bob and Milburn without new currency being issued. Short of that, someone defaults. It’s either the government or the bank.

And that is why this entire system is a glorified Ponzi scheme. There will never be enough collateral to settle all of the obligations. This is all intentional. It designed this way for a reason. It is not going to end well. And the more out of hand this gets, the worse it’s going to ultimately be when it breaks for good.

“wE cAn jUsT tAX tHe riCh tO bALaNcE tHE BuDGeT!”

^sit down and keep working on your coloring book

And if you think I’m being harsh, I’m not. The people who are supposed to understand this stuff don’t…

Look, I’ll give a cap tip to Stephanie Kelton here. The crowning achievement of her MMT documentary is that we now have this Jared Bernstein clip. That’s where my compliments will stop though because Doctor Kelton’s medicine is going to kill the patient.

The Federal Debt is not a “savings account.” It’s a balance that is owed to the country’s bond holders. The fact that savings accounts may use those bonds as collateral doesn’t magically turn United States liabilities into United States assets. If anything, we should all be very concerned that our government behaves like Lloyd Christmas.

Closing Summary

So in closing, yes, the debt is a problem. Sorry, it’s just math. I think we all have a rough idea of what the solution is probably going to be; mainly, something resembling a monetary reset where physical cash is officially eliminated and the digital currency is completely programmable. And yes, we all probably have a rough idea of what that will do for real asset prices and who it will ultimately benefit. The Stephanie Keltons of the world have a been given a platform for a reason. And it’s not to go back to sound money.

But that doesn’t mean that we can’t.

I’ll leave you with a final question to ponder this weekend…If the state just prints the money out of thin air with the help of the central bank and they want you to believe the debt doesn’t matter, why are we paying income taxes?

PS- “No Country for Old Men”…what a f*cling classic movie, huh? One of those movies I’m so thankful I went to see whilst it was playing in theatres…I still remember being on the edge of my seat the entire goddamn movie. Creepy and suspenseful, masterfully done if you ask me.

Good article, Mike. I mean the content is absolutely a total shit sandwich to consume, of course, but if I were merely seeking someone to tell me nonsense about rainbows and butterflies all day, I’d probably be subscribed to Rafifi’s Substack feed rather than yours. Whaaatt??!! Raffi isn’t on Substack, you say…??? Oh FML…