Playing The Long Game With Gold

I'm as surprised as anyone the Federal Reserve has actually managed to get the Funds Rate to 5%. I'm more surprised Gold has held up as well as it has in that hiking environment.

I stumbled upon an old post from 2022 and I couldn’t help but laugh out loud when I read the headline:

At the time, the Fed Funds rate was still on the floor. Now it’s over 5%. Turns out the Fed actually can hike and hyperbole isn’t all that helpful. The central bank people appear to be the winners. I don’t want to put any shade on that whatsoever. My “heuristics” got me to a bad place. The “fancy analytics” of the academically credentialed central bankers totally worked.

Narrator: This is Scott Adams-inspired performance art.

Joking aside, I have quite a bit of egg on my face and the degree to which I have been wrong has necessitated reflection about why I missed so badly on some of these rate hike predictions from last year. I think my main problem was ignorance for how long it takes cost of credit decisions to ripple through the economy. First off, my expectation that hiking rates would crush employment hasn’t panned out if initial jobless claims are any indication:

I published The Fed Can’t Hike on February 17th, 2022. At the time, initial claims were oscillating between 215-235k on a weekly basis. Those figures eventually fell to under 200k later in the year before spiking back up only recently. It would seem the consumer hasn’t tapped out just yet. However, we’re probably getting closer.

From a debt standpoint, there was $817 billion in credit card debt outstanding in mid-February 2022. 16 months later… $993 billion. An increase of 21.5%.

We had revolving credit expansion all the way up until the COVID crash. Then debt was suddenly paid down, in large part because of stimmy checks - the timing of which line up with spikes in the personal saving rate. But since the trough of $739 billion in CC debt in April of 2021, it’s been a straight line up in outstanding loans ever since. Simultaneously, we’re experiencing our worst sustained lows in the personal saving rate since 2008. And again, with the exception of certain tech companies, real job losses haven’t really even started yet. People are still spending, they’re just using more debt to do it. At a time when borrow rates are higher…

It’s difficult to predict timing. Getting the ultimate result right is much easier, in my humble opinion. Yes, this is the “I’m not wrong, I’m just early” excuse. Recall what I said last August in The Macro, The Fed, and The Big Trade:

We know what will happen if the Fed doesn’t pivot; debts by the public and private sector can’t be refinanced in a way that make them more serviceable. When that happens, everything collapses; stocks, bonds, and more importantly, the entire real economic system.

We saw the impact from rate hikes play out in March. Banks that borrow short (from depositors) and lend long (to the government) are/were underwater. Thanks to technology and mobile banking, the digitization of personal finance now means a bank run can happen in mere minutes and doesn’t even require leaving the sofa. What happened to the banks in March was a direct result of central bankers guiding for no rate hikes and then immediately moving from 0 to 4.5% in a year.

But again, it takes time to break things and timing is difficult to predict. My thinking has always been any tightening will be short-lived and the liquidity spigots will ultimately be turned back on through balance sheet expansion and ZIRP. What I didn’t expect was a 5% Fed Funds Rate. And I’ll willingly admit that the powers that be have done a nice job making US debt look attractive again. It’s silly to keep cash in a 0% savings account when you can grab a “risk free” 5% yield by purchasing bonds directly or by moving funds to a money market account.

But like any Proof-of-Stake crypto shitcoin; the question remains, where does the yield come from? New issuance? Or “protocol fees?” If it comes from issuance, does the yield beat the rate of inflation? I’ll capitulate here and say that I’m finished making bold predictions. But I will point out that even though my assumptions on rate hikes were wrong last year, my positioning has been mostly fine.

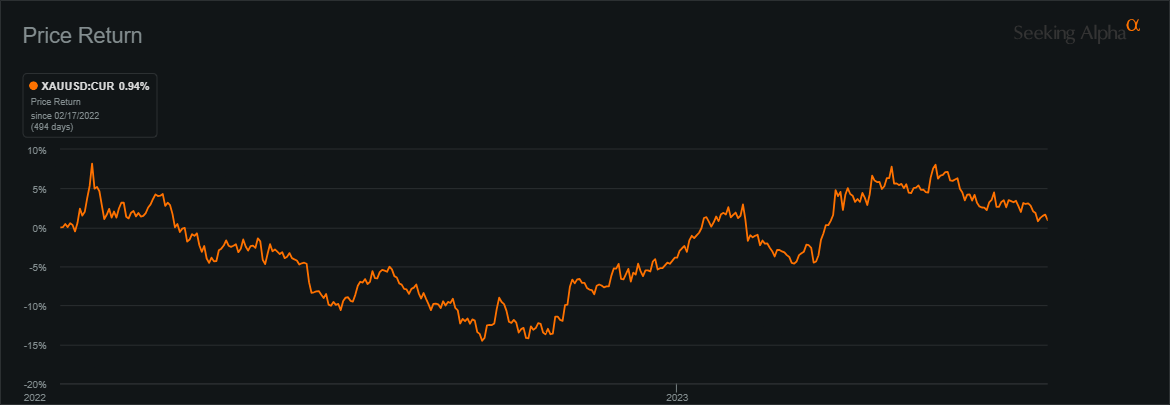

Judging again from my February 17th, 2022 proclamation that the Fed can’t hike, in the face of higher interest rates, Gold is… essentially flat. Of course, it hasn’t been in a straight line. There was a large 17% drawdown and then a sizeable rally. But with the headwind of a 500 bps surge in Fed Funds and a several hundred bps increase to the risk free rate on bonds, Gold has held up just fine. That’s very telling.

It doesn’t mean we can’t see lower prices from here. But if we’re truly playing the long game, I think we want to take note of what the central banks have been doing pertaining to gold over the last 3 quarters…

Disclaimer: I’m not an investment advisor.